A requerimiento AEAT or requerimiento de Hacienda is not just an administrative message. It is a procedural act. The way you answer can preserve the file, narrow the issue, and avoid separate penalty exposure. It can also do the opposite: miss the clock, admit facts too broadly, upload weak documents, or convert a manageable tax check into a sanction discussion.

This is especially relevant for foreign residents, founders, executives and families with international income, rental property, company distributions, crypto reporting or foreign-asset declarations. In those cases, the question is rarely only how to contestar requerimiento AEAT online. The harder question is what legal position your answer is creating. If the notice relates to Spanish income tax, it should be reviewed together with your wider income tax filing position in Spain and, where the file may lead to an appeal, with the strategy for preserving arguments before the next act is issued.

Last updated: 21 May 2026 · Based on AEAT electronic-notification guidance and the Ley General Tributaria framework checked during preparation.

Key takeaways at a glance

- Read the notice first. The notification usually tells you the procedure, the response route, the expediente/reference number and the specific documents requested.

- Do not confuse clocks. Electronic access rules, response deadlines, appeal periods and voluntary regularisation rules are different legal clocks.

- Non-response is risky. Under Article 203 LGT, failing to attend a duly notified tax request can itself become resistance, obstruction, excuse or refusal.

- Answer with evidence, not emotion. The safest response maps each requested item to a document, an explanation, or a defensible reason why the item is not available.

- A complementary return is not always the answer. Once AEAT has opened a procedure, the legal effect of filing or correcting a return needs to be checked before submitting anything.

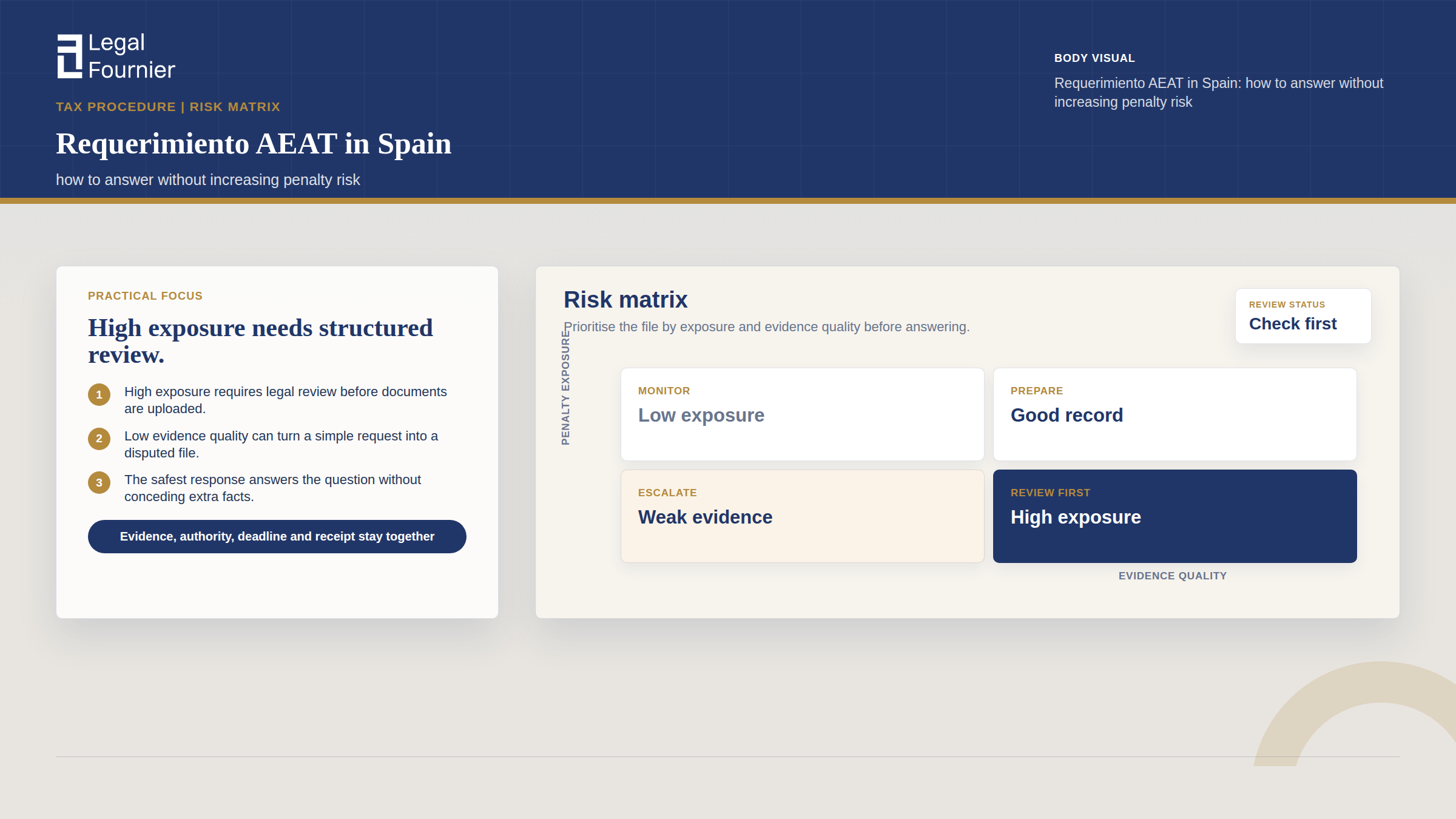

The first mistake: treating every AEAT request the same

The word requerimiento is used casually, but the document you receive may sit inside very different procedural contexts. It may be a request to provide supporting documents, a step inside a comprobación limitada, a proposal of provisional assessment, a sanction-related notice, a debt-collection act, or a request linked to a specific return such as IRPF, VAT, Modelo 720 or Modelo 721.

AEAT’s own technical guidance says to review the content of the notice before using the online response route, because some notices direct the taxpayer to a specific channel such as “Aportar documentación complementaria” or a model-specific response procedure. That is not a minor technicality. Filing through the wrong route can leave the taxpayer with proof of submission, but not necessarily with the right procedural response.

The first legal task is not to answer quickly. It is to identify what the notice is asking, what procedure it belongs to, and what legal consequence follows if the answer is incomplete.

What to extract from the notification before drafting

- Procedure type. Look for whether the file is verification, limited verification, collection, sanction, rectification, refund, census or another tax-management procedure.

- Tax, model and period. IRPF 2023, VAT Q4, Modelo 720, Modelo 721, company tax and withholding files are not answered in the same way.

- Exact request. Separate documents requested from explanations requested. A bank statement, invoice, certificate or contract is not the same as an admission about tax residence or beneficial ownership.

- Response route. Confirm whether the notice asks for a CSV-based response, a model-specific document upload, a formal allegation, a recurso, or another channel.

- Next act threatened. Many notices state what may happen if no answer is filed: provisional assessment, refusal of a refund, continuation of collection, or sanction consequences.

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

The deadline problem: access, response and appeal are different clocks

Taxpayers often ask how many days they have to answer a requerimiento. The careful answer is: read the notice and calculate the deadline from the notification date under the applicable rules. Do not rely on a generic internet answer.

For electronic notifications, Article 43 of Law 39/2015 provides that an electronic notification is considered made when the taxpayer or authorised representative accesses its content. Where electronic notification is mandatory or expressly chosen, the notice can be treated as rejected after ten calendar days from being made available if it is not accessed. AEAT also shows taxpayers pending, expired and unread electronic notices through its electronic-notification tools and DEHú environment.

That ten-calendar-day access rule is not the same as the period to answer the request. The response period is the one stated in the notice, read with the applicable procedural law. As a general administrative rule, Article 30 of Law 39/2015 treats periods expressed in days as working days unless a law or EU rule states that they are calendar days. But tax notices can have their own specific wording, and the notification itself is the first document to trust.

Why calendar mistakes become substantive problems

A late response is not merely a late upload. It can change how AEAT reads the taxpayer’s cooperation, whether the administration proceeds with the data it already holds, and whether a later appeal has a clean procedural record. If the notice is inside a comprobación limitada, Article 138 LGT requires the taxpayer who has been required to appear or provide documents to attend and produce what has been requested. Before a provisional liquidation is issued, the taxpayer normally must be given the chance to allege what is appropriate to their right.

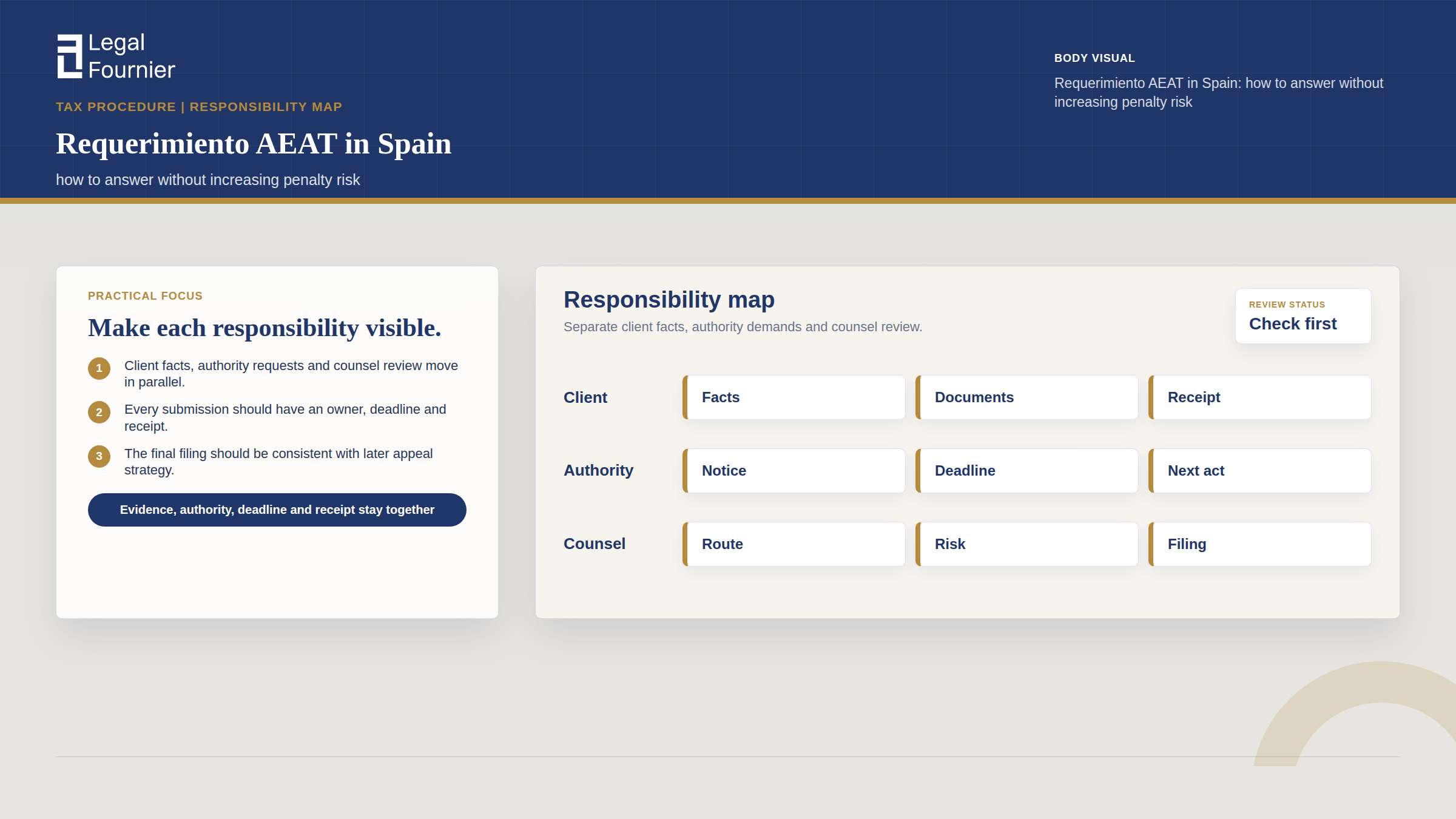

The practical point is simple: build a calendar immediately. Record the date the notice was made available, the date it was accessed, the last day to answer, any public holidays that affect the count, and the date on which the response was actually registered. The filing receipt is part of the defence file, not an administrative souvenir.

How to answer without creating separate penalty exposure

The safest response is disciplined. It answers the actual request, attaches the documents in a coherent order, and avoids introducing unnecessary statements that later conflict with the tax position. A taxpayer can damage the file by saying too little, but also by saying too much in the wrong way.

Article 203 LGT treats failure to attend a duly notified request as one possible form of resistance, obstruction, excuse or refusal to tax-administration actions. That does not mean every imperfect response will automatically produce a penalty. It does mean that silence, delay and evasive answers can become a separate issue from the underlying tax adjustment.

A defensible answer has five parts

| Part of the response | What it protects |

|---|---|

| Identification of the notice | Links the answer to the correct expediente, tax model, year and taxpayer. |

| Document index | Shows that each requested item has been addressed and makes the officer’s review easier. |

| Short legal explanation | Frames the facts without making broad admissions beyond the request. |

| Gap explanation | Explains unavailable documents, third-party delays or foreign evidence issues before they are treated as non-cooperation. |

| Receipt preservation | Preserves proof of registration, attachments and filing time for any later appeal or sanction file. |

AEAT’s online guidance confirms that, after accessing the telematic register, the taxpayer can complete fields such as expediente/reference, subject and contact details, attach files, describe the filing and then submit. If the submission is successful, the system shows a registration receipt. In practice, the receipt should be downloaded immediately together with the final PDF pack that was filed.

What not to do in the response box

Do not use the free-text box as a confession, negotiation note or emotional explanation. If there is an error, the legal work is to classify the error, decide whether it is material, determine whether a complementary or rectifying return is legally appropriate, and present the issue coherently. If the taxpayer has a defensible interpretation, the response should preserve it. If the taxpayer needs more time to collect foreign documents, the response should make that difficulty visible and support it with evidence where possible.

A good answer reduces uncertainty for the officer without giving away legal positions the notice did not require you to concede.

When the notice Is part of a comprobación limitada

Many AEAT requests sit inside a procedimiento de comprobación limitada. Article 136 LGT allows the tax administration to examine the data declared by the taxpayer, the supporting documents filed or requested, data already held by the administration, and certain official books and records. It is narrower than a full inspection, but it is still a formal tax-check procedure.

This matters because the administration may later issue a provisional liquidation based on the record. Article 139 LGT states that a limited verification procedure can end by express resolution, caducity once the maximum period has passed without notified resolution, or the start of an inspection procedure covering the same object. A weak answer at this stage can therefore shape the facts that later appear in the provisional assessment.

The strategic issue is the future file

When the request concerns income, deductions, exemptions, residence, bank movements, rental expenses, business activity, related-party payments or foreign assets, the taxpayer should assume that today’s answer may be read again in a later liquidation, sanction proposal or appeal. The response should therefore be prepared as the first layer of the future file, not as a one time upload.

For substantial or international taxpayers, this is where specialist review changes the outcome. A bank transfer may be salary, dividend, shareholder loan, sale proceeds, trust distribution, family support or reimbursed expense. AEAT may only ask for a bank statement, but the explanation attached to that statement decides how the transfer is framed.

Complementary return, rectification or allegations?

One of the most expensive mistakes is assuming that a requerimiento automatically means the taxpayer should file a complementary return. Sometimes that is correct. Sometimes it is not. Article 122 LGT regulates complementary self-assessments where the correction produces more tax to pay or a lower refund. Article 120.3 LGT regulates the rectification route where the original return harmed the taxpayer’s legitimate interests. Following Real Decreto-ley 13/2022 and the implementing regulations (notably Orden HAC/265/2024 for IRPF since 2024), both routes have been unified into a single autoliquidación rectificativa for those taxes where the regulation has activated the new model — so the technically correct route depends on the tax, the period and whether the rectifying model is already in force.

The timing is also critical. Article 27 LGT applies only to late self-assessments or declarations filed without prior administrative request. Article 27.1 LGT defines prior request broadly as any administrative action — with formal knowledge of the taxpayer — directed at the recognition, regularisation, verification, inspection, securing or liquidation of the same tax debt. Once AEAT has notified such an action for the same tax and period, the Article 27 surcharge regime is generally displaced and the issue moves inside the open procedure, where the consequence is no longer a surcharge but potential sanction.

A practical decision tree

- If AEAT only asks for evidence, the answer may be a structured document pack with a short explanation, not a new return.

- If there is an underpayment, assess whether the open notice prevents treatment as a voluntary late regularisation and whether the correction belongs in the procedure.

- If the original return harmed the taxpayer, a rectification route may be relevant, but it should not be mixed casually with a requerimiento response.

- If AEAT has proposed a liquidation, the correct move may be formal allegations before the deadline rather than simply uploading documents.

- If a sanction proposal has arrived, the response must address culpability, evidence and proportionality, not only the underlying tax calculation.

Special risk profiles for foreigners in Spain

AEAT requests become more delicate when the taxpayer’s facts do not fit a standard Spanish wage-earner file. International clients often have clean records but complex evidence. The danger is that a short Spanish response makes the file look inconsistent when it is merely international.

Foreign income and tax residence questions

A requerimiento may ask for bank movements, employment contracts, foreign payslips, certificates of tax residence, dividend statements or proof of days in Spain. These documents should be reconciled before filing. If a taxpayer claims non-residence, Beckham regime treatment, treaty relief, or exclusion of foreign income, the response must be consistent with the passport record, payroll, bank flows and prior Spanish filings.

Modelo 720, Modelo 721 and foreign assets

Foreign-asset reporting notices require particular care because the evidence often sits outside Spain and may be denominated in another currency or held through foreign institutions. If the issue concerns crypto assets abroad, the file should not duplicate general guidance on Modelo 721. The narrower point is whether the specific notice asks for ownership evidence, valuation, filing history, residence status, or an explanation of why the reporting obligation was not triggered. For background on the reporting threshold and obligation, see Legal Fournier’s existing guide to when Modelo 721 is obligatory for expats.

Companies, founders and administrators

For founders and administrators, a personal AEAT request may overlap with company accounting, related-party payments, VAT, withholding or director remuneration. The response should avoid separating the personal and corporate files too aggressively. A statement made in the personal IRPF file can later be compared with company tax, accounting records or Social Security positioning.

Representation: who should file the answer?

The taxpayer can usually answer directly where the procedure allows it, using the identification methods accepted by AEAT. A representative can also act, but the representation must be technically valid. AEAT maintains a Registro de apoderamientos for powers to carry out internet-based tax procedures, and its guidance explains that powers can be granted electronically, by personal appearance, or through a public document or notarised private document submitted to AEAT.

This is not only an access issue. If the person filing the response lacks the right power, the file can lose time precisely when timing matters. For international clients, representation should be checked as soon as the notice is accessed, not on the last day of the response period.

If AEAT issues an assessment or sanction proposal

Answering the requerimiento is not always the end of the matter. AEAT may issue a provisional liquidation, refuse a refund, start a sanction file or continue collection. At that point, the file usually shifts from document response to formal defence.

AEAT’s guidance on the online response route notes that where the notification allows a recurso or economic-administrative claim, the taxpayer must choose the correct route and know the department to which the request should be addressed. Under Article 235 LGT, an economic-administrative claim in first or sole instance is generally filed within one month from the day after notification of the challenged act. Recurso de reposición also operates as a tax-review route against eligible tax-management acts, but it should not be filed casually where a direct economic-administrative claim is strategically stronger.

The important point is that the appeal strategy starts before the appeal. If the original response is vague, late, unsupported or inconsistent, the later appeal inherits those weaknesses. If the response is structured, evidenced and legally framed, the appeal begins from a much stronger record.

A requerimiento is often the cheapest moment to fix the file. Waiting until the liquidation or sanction proposal usually narrows the options.

Frequently asked questions about contestar requerimiento AEAT

How do I answer a requerimiento AEAT online?

In many cases, AEAT allows the taxpayer or representative to answer through the electronic office using the CSV on the notification, the expediente/reference number, accepted identification and attached documents. The notice itself needs to be checked first because some procedures require a specific response route or a model-specific document upload.

How many days do I have to answer a requerimiento de Hacienda?

The deadline is the one stated in the notification, calculated under the applicable rules. Do not assume every request is ten days or that every period is counted the same way. Electronic-notification access rules, response deadlines and appeal periods are separate clocks.

Can I be fined for not answering AEAT?

Potentially, yes. Article 203 LGT treats failure to attend a duly notified tax request as one form of resistance, obstruction, excuse or refusal to tax-administration actions, and the sanction is scaled depending on whether the failure is first, second or third in respect of the same request, and on whether the information relates to the obligor’s own activity or to third parties. Whether a penalty is finally imposed depends on the facts, the procedure and the conduct of the taxpayer.

Should I file a complementary return after receiving the notice?

Not automatically. Complementary returns have a specific function under Article 122 LGT, and voluntary late-filing treatment under Article 27 LGT depends on absence of prior request. Once AEAT has notified a procedure, the correction strategy should be checked before filing a new return or self-assessment.

What if I cannot obtain a foreign document before the deadline?

Do not stay silent. A defensible response usually identifies the requested document, explains why it is temporarily unavailable, attaches proof of the request to the foreign bank, employer or authority, and provides any alternative evidence that supports the position. Whether an extension or later completion is possible depends on the specific procedure and notice.

Conclusion: answer the procedure, not just the portal

The AEAT portal is only the filing mechanism. The real work is procedural and evidentiary: classify the notice, calculate the correct deadline, decide whether the issue is documentary or substantive, and prepare a response that preserves the taxpayer’s position if the file later becomes a liquidation, sanction proposal or appeal.

For simple notices, that may mean a clean document pack and proof of filing. For international taxpayers, founders, families and investors, it often requires a broader tax-risk review before anything is uploaded. The cost of a careful response is usually lower than the cost of trying to repair a file after the administration has already interpreted the facts against the taxpayer.

Legal Disclaimer. This article is provided for informational purposes only and does not constitute legal advice. Every case involves specific facts and circumstances that may affect the outcome. Legal Fournier recommends seeking professional legal guidance before taking any action based on the information contained herein.