Getting your head around home insurance in Spain—what the locals call seguro de hogar—is an essential first step to settling in. Think of it less as a piece of paper and more as a financial safety net, built to protect your home's structure and everything you've put inside it.

Let’s break down what that actually means.

What Exactly Is Home Insurance in Spain?

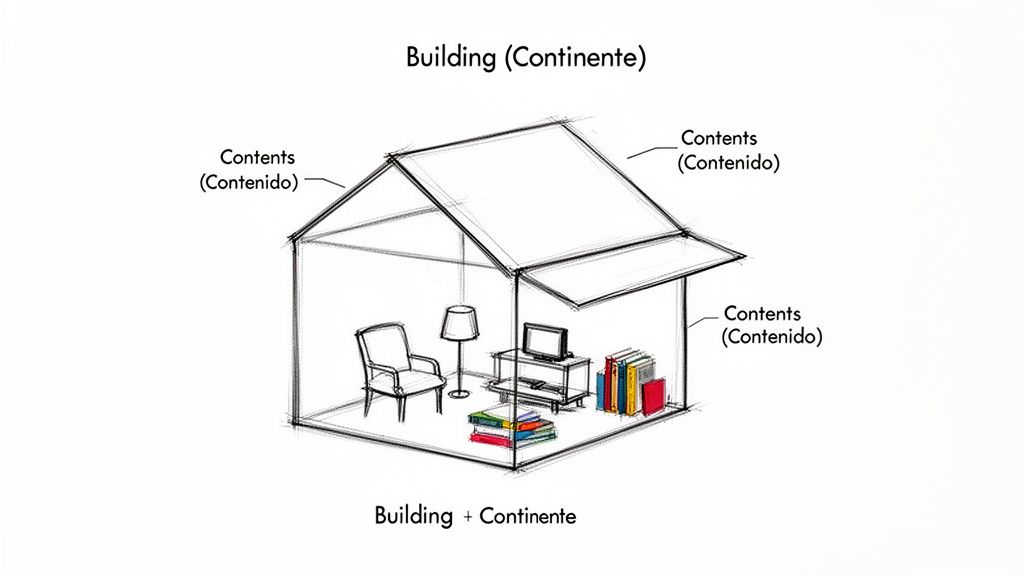

The easiest way to understand Spanish home insurance is to imagine your home is a simple shoebox. The policy has two distinct parts that work together.

First, you have the continente. This is the shoebox itself: the walls, roof, floors, and anything permanently fixed to the structure. We’re talking about built-in wardrobes, your kitchen counters, and the bathroom plumbing. It’s the physical shell of your property.

Then, there's the contenido. This is everything you decide to put inside the shoebox. It covers all your personal belongings: furniture, clothes, laptops, jewellery, you name it. This is the part of the policy that protects your stuff from theft or damage.

Why Both Parts Matter for You

This distinction isn't just jargon; it’s important whether you own or rent. Homeowners obviously need to insure both the continente and the contenido to be fully covered. But where we see expats trip up most often is when they're renting. Many incorrectly assume that their landlord's insurance has them covered. It doesn’t.

A landlord's policy protects the building (continente). As a tenant, you are entirely responsible for insuring your own belongings (contenido) and your personal liability. Without it, you have zero financial protection if your things are stolen or damaged in a fire.

This is why getting your own policy as a renter is non-negotiable. It covers your valuables and almost always includes civil liability insurance (responsabilidad civil), which is needed if you, say, accidentally leave a tap running and flood your downstairs neighbour’s flat.

To help you get familiar with the terms you'll see on a policy document, here's a quick reference table.

Key Home Insurance Terms at a Glance

| Spanish Term | English Translation | What It Covers |

|---|---|---|

| Continente | Building/Structure | The physical structure: walls, roof, floors, and fixed installations. |

| Contenido | Contents | Your personal belongings inside the home: furniture, electronics, clothing, etc. |

| Responsabilidad Civil | Civil Liability | Damage or injury you accidentally cause to third parties (e.g., your neighbour). |

| Prima | Premium | The amount you pay for your insurance policy (monthly, quarterly, or annually). |

| Póliza | Policy | The official insurance contract document. |

| Siniestro | Claim | The event that triggers an insurance claim, like a theft or water damage. |

| Franquicia | Deductible/Excess | The amount you pay out-of-pocket on a claim before the insurer pays the rest. |

Knowing these seven terms will put you miles ahead when comparing quotes and reading your final policy.

The good news is that the Spanish insurance market is robust and growing, giving you more competitive options. The country's non-life insurance market was valued at USD 98.50 billion in 2025 and is set to expand further. For you, that means more choice and better products tailored to modern needs. You can dig into more data about the Spanish insurance market to see the trends.

A solid seguro de hogar is about buying peace of mind. It ensures that a disaster like a burst pipe, a kitchen fire, or a break-in doesn't become a financial catastrophe, letting you build your new life in Spain on a secure foundation.

Right, let's get straight to it. Do you actually need home insurance in Spain by law?

The short answer is: it depends. For most expats, though, it’s either a legal must-have or just plain common sense. We see a lot of confusion on this point, so let's clear it up.

The law is crystal clear for anyone buying with a mortgage. Spanish banks will not release the funds for your loan unless you have a valid building insurance policy in place. This is called seguro de hogar, and it must, at a minimum, cover the continente (the structure of the building).

Why? It’s simple. The bank is protecting its investment. If a fire, flood, or anything else catastrophic were to destroy the property, they need to know their loan is covered. Without that basic insurance, their asset, your home, is worthless, leaving them with an unpaid loan.

The Bank Policy Trap

Now, here’s a critical piece of advice we give all our clients. When you get your mortgage, the bank will almost certainly try to sell you their own insurance policy. It's often overpriced, and they'll present it as just another part of the package deal, sometimes making it sound like you have no other choice.

You are not obligated to buy the bank's insurance. Spanish law is explicit: you have the right to choose your own provider. In our experience, shopping around for home insurance can save you hundreds of euros every single year compared to the bank's bundled offer.

Don't let them pressure you. You can politely decline their policy and find a much more competitive quote from an independent insurer. All you have to do is show the bank proof of your alternative policy that meets their minimum requirements for the continente.

What About Renters and Cash Buyers?

If you've bought your property outright with cash or you're renting, there's no law forcing you to get home insurance. But going without it is a huge financial gamble, one we would strongly advise against. This is especially true for tenants.

As a renter, your landlord’s insurance covers the building (continente), but it does absolutely nothing for you personally. It won’t cover your furniture, your laptop, or your liability if something goes wrong.

Let’s walk through a scenario we see all too often:

Imagine a pipe bursts in your rented apartment while you're out. The water ruins your computer and sofa, then leaks through the floor, destroying the ceiling of your neighbour's flat below.

- Without contenido (contents) insurance, you're on the hook for replacing all of your own damaged belongings.

- Without responsabilidad civil (civil liability) insurance, you could be held personally liable for the thousands of euros it costs to repair your neighbour's apartment.

This is exactly why a good home insurance policy is a smart, non-negotiable move for renters. It protects your stuff and shields you from liability claims that could be financially devastating. For anyone navigating the process of settling in, understanding these liabilities is just as important as securing the right to live here. You can explore more about what's involved in our guides to obtaining Spanish residency.

Decoding Your Policy: What Coverage to Look For

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

Alright, you've grasped the difference between continente (the building) and contenido (your stuff). Now for the important part: figuring out what a good policy actually protects you from. A rock-bottom premium might satisfy your mortgage lender, but it can leave you dangerously exposed when something actually goes wrong.

We’ve seen it happen time and again: expats skim the details, only to discover their coverage has massive holes right after a disaster. Let's break down what you absolutely need, what you should consider for Spain’s unique environment, and the extras that are genuinely worth the money.

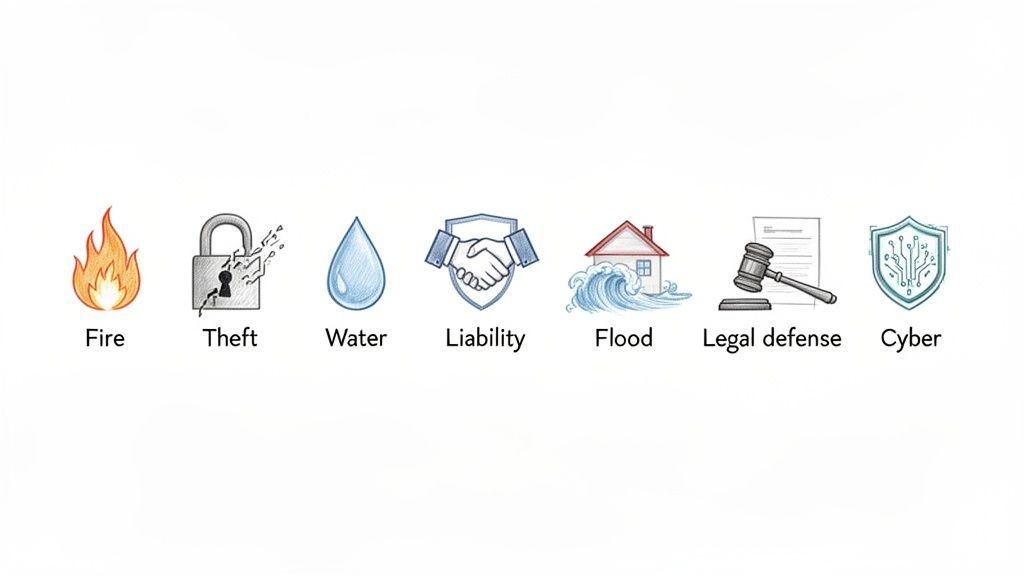

Core Protections You Cannot Skip

Think of these as the non-negotiables. If a policy you're looking at is missing any of these, it's a major red flag.

Responsabilidad Civil (Civil Liability): This is arguably the most important part of your policy. It covers you if you, a family member, or even your pet accidentally harms someone or damages their property. Your bathtub overflows and floods your downstairs neighbour? This is what pays for their ruined ceiling and floors. Most policies start around €150,000, but we strongly suggest aiming for €300,000 or more. It costs very little extra for a lot more peace of mind.

Daños por Agua (Water Damage): This covers damage from burst pipes, leaky radiators, or malfunctioning appliances inside your own home. Water damage is one of the most common claims filed in Spain, making this coverage absolutely essential. It should pay for finding the source of the leak and repairing the resulting damage to your walls, floors, and belongings.

Incendio y Explosión (Fire and Explosion): This is standard in every policy for a reason. It covers damage from fire, lightning strikes, and explosions, protecting both the structure (continente) and your possessions (contenido).

Robo (Theft): This covers your belongings if someone breaks into your home. Read the fine print here. Insurers distinguish between robo (theft with forced entry, like a smashed window) and hurto (theft without force, like someone snatching a wallet from an unlocked house), which often isn't covered. A good policy also covers the damage caused during the break-in itself, like a shattered door frame.

Coverage for Spain’s Unique Risks

Spain is more than just sunshine. Its varied climate and geography bring specific risks that need specific coverage. The insurance market here is shaped by this reality, with demand for specialised products growing after major events like the devastating floods in Valencia. You can find out more about Spain's evolving insurance landscape to see how insurers are responding.

Depending on where you live, the standard "acts of God" coverage might not cut it. You have to check if you need to add specific protections for the environmental risks common to your region.

Make sure your policy properly addresses these:

- Phenomena Atmosféricos (Atmospheric Phenomena): This is for damage from severe wind, rain, snow, or hail. But there's a catch. Insurers set thresholds, meaning winds might have to exceed 80-90 km/h before the coverage kicks in.

- Inundación (Flooding): Basic policies often have very limited flood protection. If you're in a coastal town, near a riverbed, or in an area prone to the infamous gota fría (violent autumn downpours), you need to be sure your policy has robust flood coverage. This is often ultimately handled by a national body, the Consorcio de Compensación de Seguros, but your private policy is the first and necessary step to making a claim.

Smart Add-Ons That Offer Real Value

Beyond the absolute basics, a few optional extras can save you from major headaches. We usually recommend these to build a truly comprehensive safety net.

Defensa Jurídica (Legal Defence): This add-on is a lifesaver. It gives you access to legal advice and covers costs if you end up in a dispute with a neighbour, your building's community (comunidad), or even your landlord. It's an inexpensive extra that can save you thousands in legal bills.

Asistencia en el Hogar (Home Assistance): Often included in better policies, this provides a 24/7 hotline for emergency tradespeople. Locked out? Pipe burst in the middle of the night? They'll send a locksmith or plumber right away.

Todo Riesgo Accidental (All-Risk Accidental Damage): This is a fantastic upgrade that covers damage you cause to your own things. Spill red wine on that new white sofa? Accidentally knock over your 65-inch TV? This is the coverage that pays to fix or replace it.

By getting familiar with these different layers of coverage, you can move beyond just buying a piece of paper and build a policy that provides genuine security. You'll be able to read any quote and know exactly what you’re paying for, avoiding the common and costly mistake of being underinsured.

We can handle the initial paperwork like getting your NIE or residency sorted. For advice tailored to your specific situation, contact us for a consultation.

Estimating Your Home Insurance Costs

So, what’s the real cost of home insurance in Spain? Let's get straight to the numbers and what drives them. The good news is that most expats find comprehensive coverage here surprisingly affordable.

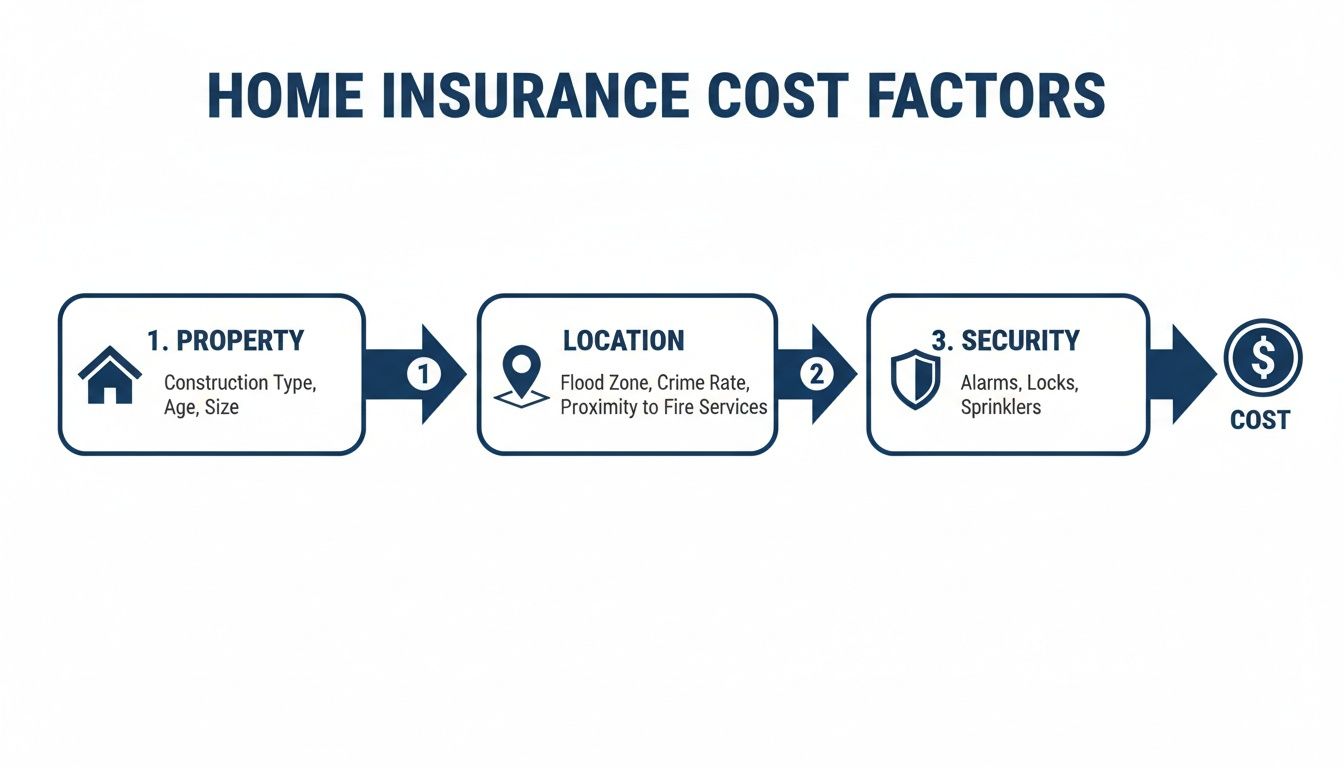

The price of your policy, known as the prima, isn't just a number pulled from a hat. Insurers calculate it based on the specific risk profile of your property. They’re essentially asking: how likely are you to make a claim, and what would it cost us?

Key Factors That Influence Your Premium

Getting a handle on these variables is the first step to making sure you get a fair price. Insurers look at a few core elements:

Property Type and Size: It’s simple maths. A large, detached villa in the countryside has more potential issues and more entry points for a burglar than a 90m² apartment in a secure city building. The bigger the property (continente), the higher the risk.

Location: Your postcode matters. A ground-floor flat in a busy city neighbourhood might face a higher theft risk, while a beachfront property on the Costa Brava will have premiums factoring in potential storm damage. Insurers have incredibly detailed data on crime and climate risks for every single region.

Construction Quality: The age and materials of your home are a big deal. A modern build with brand new plumbing and electrics is a much safer bet against fire or leaks than a charming, 200-year-old village house with its original wiring.

Declared Value of Contents (Contenido): This is a huge one. The more your belongings are worth, the more it costs to insure them. It's absolutely critical to take the time to create a realistic inventory of your furniture, electronics, and valuables. Get this wrong, and you risk being underinsured when you need it most.

To give you a concrete idea, a standard comprehensive policy for a 90m² apartment in a major city like Madrid or Valencia typically lands somewhere between €250 and €400 per year. For a larger 150m² villa with a garden, you’re more likely looking at €400 to €700 annually, depending on the specifics.

How to Actively Lower Your Insurance Costs

You’re not powerless here. You can take practical steps to make your home a lower risk for insurers, and they'll reward you with lower premiums.

Installing proper security features is the fastest way to a discount. Insurers love to see:

- An Alarm System (Alarma): A professionally monitored alarm is the single biggest deterrent to theft. It can easily knock up to 20% off your premium.

- A Reinforced Door (Puerta Blindada): A common feature in Spain for a reason. A high-security front door makes a break-in significantly harder.

- Window Grilles (Rejas): An absolute must for ground-floor apartments and accessible villas. They are an effective and visible security layer.

- A Safe (Caja Fuerte): If you have high-value jewellery or documents, storing them in a professionally installed safe will also help lower your costs.

In our experience, the upfront cost of installing a good puerta blindada or an alarm system often pays for itself within just a few years through the annual savings on your insurance premium. Think of it as an investment in both your peace of mind and your wallet.

Sample Annual Home Insurance Premiums in Spain

To give you a clearer picture, this table breaks down some typical annual costs. Use it as a starting point to budget for your own property.

| Property Profile | Basic Coverage (Building + Liability) | Comprehensive Coverage (Building + Contents + Add-ons) |

|---|---|---|

| 70m² Apartment in Valencia City Centre | €180 – €250 | €250 – €380 |

| 120m² Townhouse on the Costa Blanca | €250 – €350 | €380 – €550 |

| 200m² Villa with Pool near Marbella | €350 – €500 | €550 – €800+ |

As you can see, the price varies, but it's manageable. It's all about finding the right balance between robust coverage and a price that makes sense for you.

If you have questions about your specific property or need help with the associated paperwork for your move, our team is here to provide clarity. We handle the complex legal and administrative side of things so you can focus on settling in.

How to Get Your Policy as an Expat

Sorting out home insurance in Spain isn’t the bureaucratic headache you might be picturing. It's actually quite straightforward, but only if you have your documents in order from the very beginning. Let's walk through the exact steps, from gathering your papers to making the final payment.

Your Essential Document Checklist

Before you can even get a quote, you’ll need to have a few key documents ready. In our experience handling paperwork for expats across Spain, the single biggest delay is a missing NIE. Getting that sorted first makes everything that follows run ten times smoother.

- NIE (Número de Identidad de Extranjero): This is your foreigner identification number. It's non-negotiable for almost any contract in Spain, including insurance. We help clients secure their NIEs every day, turning a potential hurdle into a simple first step.

- Passport: You'll need your valid passport as your main photo ID.

- Proof of Property: This will either be your rental contract (contrato de alquiler) if you're a tenant, or the title deed (nota simple) if you've bought your place.

Having these three things on hand will speed up the entire process dramatically.

Overcoming the Language Barrier

The language barrier can cause a lot of stress. It is absolutely vital that you never sign a legal contract you don’t fully understand. The good news? Many major Spanish insurers have woken up to the large expat market and now offer policies, documents, and customer service entirely in English.

When you're shopping around, make a point to ask if they provide a full English-language version of the policy (póliza). This isn’t just for convenience; it’s to ensure you know precisely what’s covered and what’s excluded before you commit. This image breaks down the core factors that will shape your insurance costs.

As you can see, an insurer's calculation always boils down to your property, its location, and the security you have in place.

The Quoting and Buying Process

Once your documents are in hand, buying your policy is pretty simple. It generally works like this:

- Gather Quotes: Reach out to several insurers or use a comparison site. Give them accurate details about your property’s size, age, location, and the value of your contents to get a solid quote.

- Compare the Details: Don't just glance at the final price. Look closely at the coverage levels for liability (responsabilidad civil), the deductibles (franquicias), and any special add-ons included in the offer.

- Finalise the Contract: When you've picked a policy, the insurer will send over the final contract. Read it carefully. When looking to secure your home insurance in Spain, understanding the role of an insurance agency can be beneficial, as they can often help explain these details.

- Set Up Payment: Payment is almost always handled by direct debit (domiciliación bancaria) from a Spanish bank account. You'll need to provide your IBAN to get this set up.

We often see clients get stuck on the initial administrative steps, like getting the NIE or opening a bank account. These are foundational tasks for your entire move to Spain, not just for insurance.

Getting these things right from the start means you can secure not only your home but also handle other essentials like utilities and residency paperwork without a hitch. If you're planning your move, our comprehensive guide on the essentials of relocating to Spain can help you organise these first steps.

Navigating the paperwork for a new life abroad is what we do. If you need a hand with your NIE or any other legal documentation, we can manage the whole process for you efficiently.

Filing a Claim When Something Goes Wrong

So, the worst has happened. A pipe has burst, or you've come home to a break-in. This is exactly why you bought insurance. Knowing what to do next can turn a potential nightmare into a manageable process. The Spanish word for an insurance claim is siniestro, and handling one is all about acting quickly and methodically.

Your absolute first priority is to stop things from getting worse. If a pipe is gushing water, find the main valve and shut it off. If there's been a burglary, make sure the property is secure. Your safety comes first.

Your Immediate Action Plan

Once you've contained the immediate problem, the clock starts ticking. Your insurer needs information, and they need it fast.

Call Your Insurer Immediately: Find their 24/7 claims hotline. This call officially opens your case file and gets you a claim number. You typically have a seven-day window to report a claim, so don't put this off.

Document Absolutely Everything: Pull out your phone and become a crime scene investigator. Take dozens of photos and videos of the damage from every conceivable angle. For water damage, show where the leak started and the path it took. For a theft, photograph the broken lock or window, and the empty spaces where your things used to be.

File a Police Report (Denuncia): This is non-negotiable for theft or vandalism. Head to the nearest Policía Nacional or Guardia Civil station to file a denuncia. Your insurer won't even look at a theft claim without a copy of this official report.

In our experience helping clients, claims that are thoroughly documented right from the start get resolved much faster and with far fewer headaches.

The Assessment and Resolution Process

After your initial report, the insurance company's machine kicks into gear. The next person you'll likely meet is the assessor, known as a perito. This is an independent expert hired by the insurer to verify the damage.

The perito's job is to inspect the property, review your photos, and confirm that what happened is covered by your policy. They then write a detailed report for the insurance company. Make sure you're there for their visit. Be helpful, answer their questions, and walk them through exactly what happened.

Your claim will be settled in one of three ways: the insurer will repair the damage, replace the stolen or broken items, or give you a cash payment. The final decision rests with them, based on the perito's report and your policy details.

If your Spanish isn't fluent, this part of the process can be incredibly stressful. When you're trying to explain what happened, understanding the official forms and terminology is important. Professional insurance claim form translation can be a lifesaver, ensuring nothing gets lost in communication.

Once the assessment is done, the insurer will notify you of their decision. If they approve the claim, they'll either send their own approved repair team, arrange for replacement items, or deposit the assessed value into your bank account.

The whole thing, from that first frantic phone call to the final resolution, can take a few weeks or even a couple of months for more complicated claims. Your best defence is to keep a detailed record of every call, email, and document. If you hit a wall or find yourself in a dispute over the property, we can provide the legal support you need. Contact us for personalized advice.

Your Top Questions About Spanish Home Insurance

When you're new to the Spanish property market, a few common questions always come up. Here are the straight answers we give our clients, helping them sort out their insurance with more confidence.

Do I Really Need an NIE to Get Insurance?

Yes, you absolutely do. The NIE (Número de Identidad de Extranjero) is the key that unlocks almost every official transaction in Spain, from opening a bank account to signing a property deed. Getting insurance is no different.

Insurers won't even start the process without it. It's a non-negotiable, foundational piece of your life in Spain. If you're just at the beginning of your journey, getting this sorted first will save you endless headaches later on. Check out our guide on what the NIE is and why you need it to get started.

Can I Insure a Holiday Home I Don't Live in Year-Round?

Of course. Spanish insurers are completely used to dealing with holiday homes and second residences. It's a massive part of the market here.

The important thing is to be upfront about how you use the property. A home that sits empty for months at a time has a different risk profile. Think undetected water leaks or break-ins that go unnoticed for weeks. Because of this, your premium might be a bit higher. The insurer will also likely insist on certain security measures like a monitored alarm system or reinforced doors before they’ll agree to cover you.

What’s the Big Deal About Being Underinsured?

This is a classic and potentially very expensive mistake. People often try to lower their premium by undervaluing their contents (contenido), but this backfires badly when you need to make a claim thanks to something called the "proportional rule" (regla proporcional).

Here's how it works: Let's say you insure your belongings for €15,000, but their actual replacement value is €30,000. You've only insured them for 50% of their true worth. If a fire then causes €10,000 worth of damage, the insurance company will only pay out 50% of your claim: just €5,000. You’re left to find the other €5,000 out of your own pocket.

It really pays to be accurate. Take the time to create a detailed inventory of your belongings to get a realistic valuation. It feels like a chore, but it prevents a nasty shock right when you need your insurance to come through for you.

Sorting out the legal and administrative side of your new home in Spain can feel overwhelming. At Legal Fournier, we offer clear, expert guidance on everything from property paperwork to residency permits and tax planning. If you need a hand making sure your move is as smooth and compliant as possible, we’re here to help.