So, you’re moving to Spain. Beyond the sunshine and tapas, you'll need to get to grips with the Spanish tax system. The most important acronym to learn is IRPF.

IRPF, or Impuesto sobre la Renta de las Personas Físicas, is Spain's personal income tax. Think of it as the equivalent of the UK's PAYE or the US federal income tax. If you're a tax resident in Spain, you’re taxed on your worldwide income—not just what you earn within Spanish borders.

What Is IRPF and How Does It Affect You in Spain?

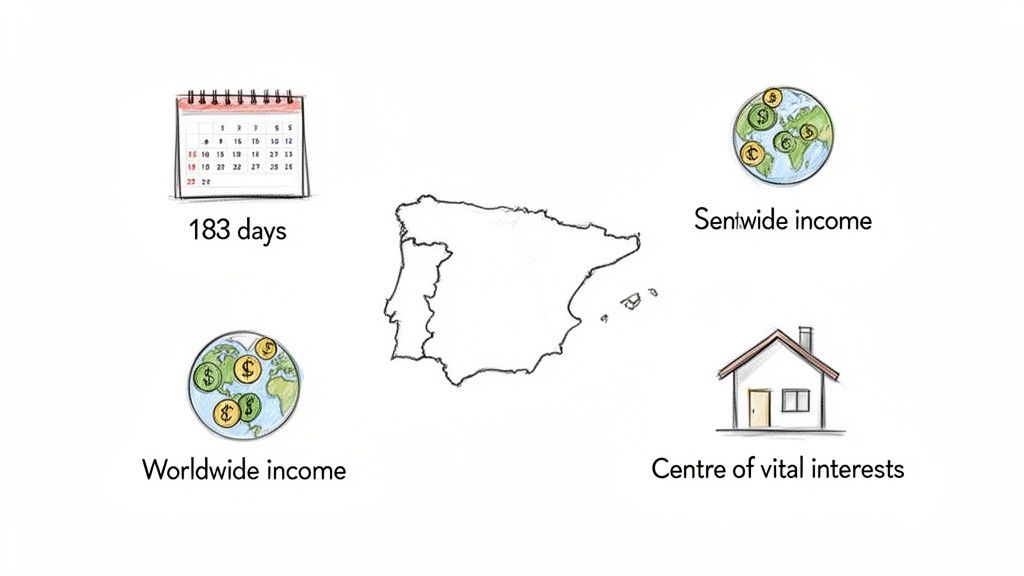

Understanding IRPF is non-negotiable for any expat, digital nomad, or professional building a life here. It’s the framework that dictates your financial obligations. The single most important question you need to answer is: are you a tax resident?

The Spanish Tax Agency (Agencia Tributaria) doesn't leave this to chance. It has clear criteria, and meeting just one is enough to classify you as a resident for tax purposes.

The 183-Day Rule

This is the most straightforward test. If you spend more than 183 days in Spain during a single calendar year (1st January to 31st December), you are automatically a tax resident. Simple as that.

These days don’t have to be consecutive. Temporary trips abroad don't stop the clock unless you can prove your tax residency is elsewhere. In our experience, this is the rule that catches most new arrivals.

Your status as a tax resident is the key that unlocks your IRPF obligations. It shifts your tax liability from only Spanish-sourced income to your entire global earnings, making it a critical distinction to understand from day one.

Centre of Vital or Economic Interests

But what if you spend less than 183 days here? You're not necessarily off the hook. You can still be deemed a tax resident if your main "centre of interests" is in Spain. This breaks down into two core concepts:

Centre of Vital Interests: This kicks in if your spouse and/or dependent minor children live in Spain. The law presumes your home base is with your family, even if your work has you travelling constantly.

Centre of Economic Interests: This looks at where your professional life is based. If the bulk of your income-generating activities or business interests are managed from Spain, the tax authorities will likely consider you a resident.

Quick Guide to Spanish Tax Residency

To make it easier, here's a simple table to help you quickly assess your own situation. If you answer "Yes" to any of these, you are likely a Spanish tax resident.

| Criteria | Condition for Tax Residency |

|---|---|

| Physical Presence | You spend more than 183 days in Spain during a calendar year. |

| Centre of Vital Interests | Your spouse or dependent minor children reside in Spain. |

| Centre of Economic Interests | The main hub of your professional activities or income-generating assets is located in Spain. |

These rules can have nuances. You can dive deeper into the specifics in our complete guide to Spain tax residency.

For anyone at the beginning of their expat journey, getting some general guidance on preparing for your move abroad is a good starting point before tackling country-specific financials like IRPF.

Figuring out your residency status is the first step. If you're unsure how these rules apply to your unique situation, contact us for personalized advice.

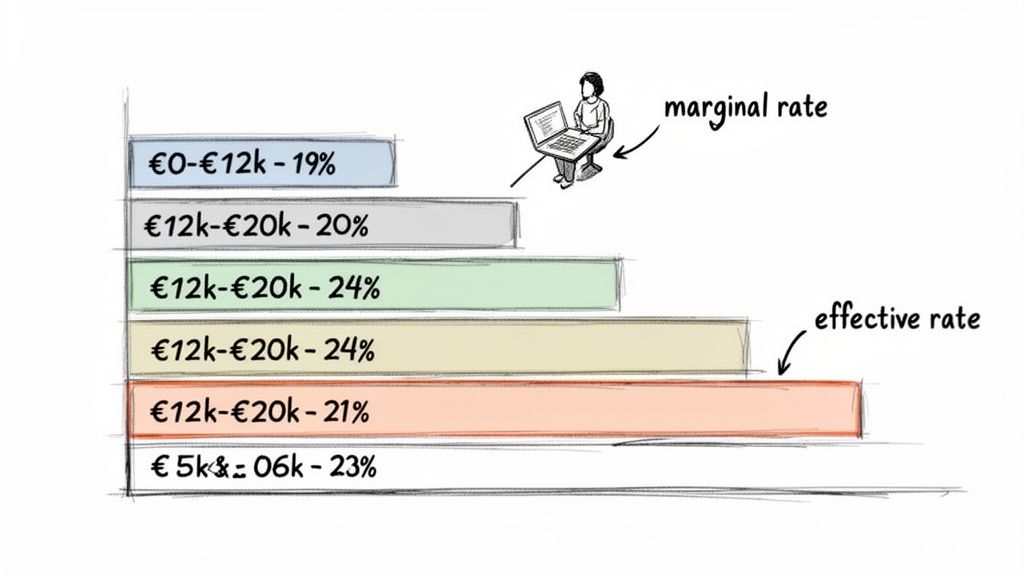

Understanding Spain's Progressive IRPF Tax Brackets

So, you've figured out you're a Spanish tax resident. The next question is: how much tax will you actually pay? Spain's IRPF system is progressive, meaning the more you earn, the higher the percentage of tax you pay.

Think of your income like filling a series of buckets. The first bucket is small and taxed at a low rate. Once it's full, your income spills into the next bucket, which is taxed at a slightly higher rate, and so on.

Many people miss this: you are never taxed on your entire salary at the highest rate you reach. Only the slice of your income that falls into that top bracket gets that higher percentage. It's the difference between your marginal tax rate (the rate on the last euro you earn) and your effective tax rate (your total tax bill divided by your total income), which is always lower.

The National IRPF Tax Bands

The IRPF is a hybrid tax, split between the state and the autonomous region where you live. While regions can adjust their half, the national brackets give you a solid baseline.

Spain's personal income tax, the IRPF, uses a set of progressive bands. For 2025, the national brackets start at 19% for the first €12,450 of income, climbing to 45% for earnings over €60,000. You can review the official 2025 IRPF tax bands for Spain.

Here’s a simple breakdown of the state-level tax bands for 2025:

- Up to €12,450: 19%

- From €12,451 to €20,200: 24%

- From €20,201 to €35,200: 30%

- From €35,201 to €60,000: 37%

- Over €60,000: 45%

Keep in mind, this is just the national half. Your final tax bill will be a combination of this and your region's specific rates.

A Practical Example: A Remote Worker's IRPF Calculation

Let’s see how this works. Imagine a digital nomad living in Valencia, earning €40,000 a year after all deductions are taken. Here’s how the state portion of their IRPF would be calculated:

First Bracket (€0 – €12,450): The first part of their income is taxed at 19%.

€12,450 x 0.19 = €2,365.50

Second Bracket (€12,451 – €20,200): The next €7,750 of income is taxed at 24%.

€7,750 x 0.24 = €1,860

Third Bracket (€20,201 – €35,200): The next chunk, €15,000, is taxed at 30%.

€15,000 x 0.30 = €4,500

Fourth Bracket (€35,201 – €60,000): The final piece of their salary, €4,800 (€40,000 – €35,200), falls into this bracket and is taxed at 37%.

€4,800 x 0.37 = €1,776

To get the total state-level tax, you just add up the tax from each bracket:€2,365.50 + €1,860 + €4,500 + €1,776 = €10,501.50

In this scenario, the worker's marginal tax rate is 37% because that's the highest rate their income touched. But their effective tax rate is much more reasonable: (€10,501.50 / €40,000) x 100 = 26.25%.

This shows you aren't paying 37% on all €40,000. In our experience, once clients grasp this layering concept, the Spanish tax system becomes much less intimidating.

Regional Tax Differences: Madrid vs. Barcelona and Beyond

One surprise for people moving to Spain is that your tax bill isn't set by the national government alone. Spain is a decentralised country, and its 17 autonomous communities hold power over their own tax policies.

This means the city you choose can dramatically change how much income tax you pay.

Your total IRPF rate is a cocktail of two ingredients: a state portion and a regional portion. While the national government sets its half of the tax bands, each region is free to tinker with its half. This has created a competitive landscape where some regions, like Madrid, intentionally lower taxes to pull in talent, while others, like Catalonia, keep rates higher to fund public services.

We see this daily: the gap in tax liability between living in Madrid versus Barcelona can easily be thousands of euros a year, especially for higher earners. Your official residence, locked in by your empadronamiento (town hall registration), is the deciding factor.

Madrid: The Tax-Friendly Hub

The Community of Madrid has worked to brand itself as one of Spain's most attractive regions from a tax perspective. It offers lower IRPF rates across most income brackets compared to other economic centers like Barcelona. For professionals and business owners, this translates into more money in your pocket.

Madrid's real advantage is its approach to wealth tax (Impuesto sobre el Patrimonio). The region offers a 100% relief on this tax, effectively wiping it off the books for its residents. This makes it a magnet for anyone with significant assets who would face a hefty annual bill in most other parts of Spain.

Catalonia: A Higher Tax Jurisdiction

Catalonia, home to Barcelona, is on the opposite end of the spectrum. The regional government enforces some of the highest IRPF rates in the country, hitting middle and high-income earners the hardest. This funds a high standard of public infrastructure, but it's a critical financial calculation.

Unlike Madrid, Catalonia fully applies the wealth tax. Rates climb from 0.21% to 2.75% on net assets above the regional allowance, adding another significant tax burden. This contrast in both income and wealth tax is why proper tax planning is non-negotiable before you choose your base in Spain.

Choosing between Madrid and Barcelona is about more than lifestyle. Your choice of city can directly impact your finances by thousands of euros each year. It’s a factor we always put front and center in our clients' relocation plans.

The strategic opportunities these regional IRPF differences create are huge. A 2025 comparison shows Catalonia's tax bands run from a 20% minimum up to 50%. For someone earning €50,000, this could mean a tax bill of around €15,100.

This is why, for many people moving to Barcelona, special regimes like the Beckham Law, which caps tax at 24% for qualifying foreigners, become so valuable. You can see a more detailed breakdown of regional tax differences on movingtospain.com.

IRPF Tax Liability Comparison (Catalonia vs. Madrid)

To see how this plays out, let's compare some approximate annual tax bills. These are estimates and your personal situation will cause them to vary, but they paint a clear picture.

| Annual Income | Approx. Tax in Catalonia | Approx. Tax in Madrid |

|---|---|---|

| €40,000 | €8,900 | €8,200 |

| €70,000 | €20,500 | €18,800 |

| €120,000 | €44,000 | €40,500 |

As you can see, the gap widens as income goes up. For a high-earning professional, the difference is impossible to ignore. This regional element is a perfect example of why generic advice on Spanish taxes often falls short.

If you’re deciding where to base yourself in Spain and want to understand the full tax implications, contact us for a personalized analysis. We can help you model the real numbers for different cities before you make a move.

Common IRPF Deductions and Allowances for Expats

Knowing how much income is taxable is only half the battle. The other half is knowing how to legally shrink that number. The Spanish tax system has deductions and allowances that can lower your final IRPF bill.

But you have to claim them. Forgetting is like leaving money on the table. Think of these deductions as tools to chisel down your taxable base before those progressive tax rates touch it. Smart tax planning means using every tool you're entitled to.

Personal and Family Minimums

First, the basics. Every tax resident in Spain gets a personal minimum allowance (mínimo personal y familiar). This is a chunk of your income that the government agrees shouldn't be taxed, simply to cover living costs.

- The standard personal minimum for anyone under 65 is €5,550 a year.

- That amount bumps up to €6,700 once you hit 65.

- For those over 75, it rises again to €8,100.

Your family situation can reduce your taxable income even further. If you have dependents living with you who earn less than €8,000 per year, you can claim additional allowances.

- For Dependent Children: The allowance is €2,400 for your first child and increases for each additional child.

- For Dependent Ascendants (Parents/Grandparents): If you're caring for a parent or grandparent over 65, you can claim an extra €1,150.

Key Deductions for Residents and Freelancers

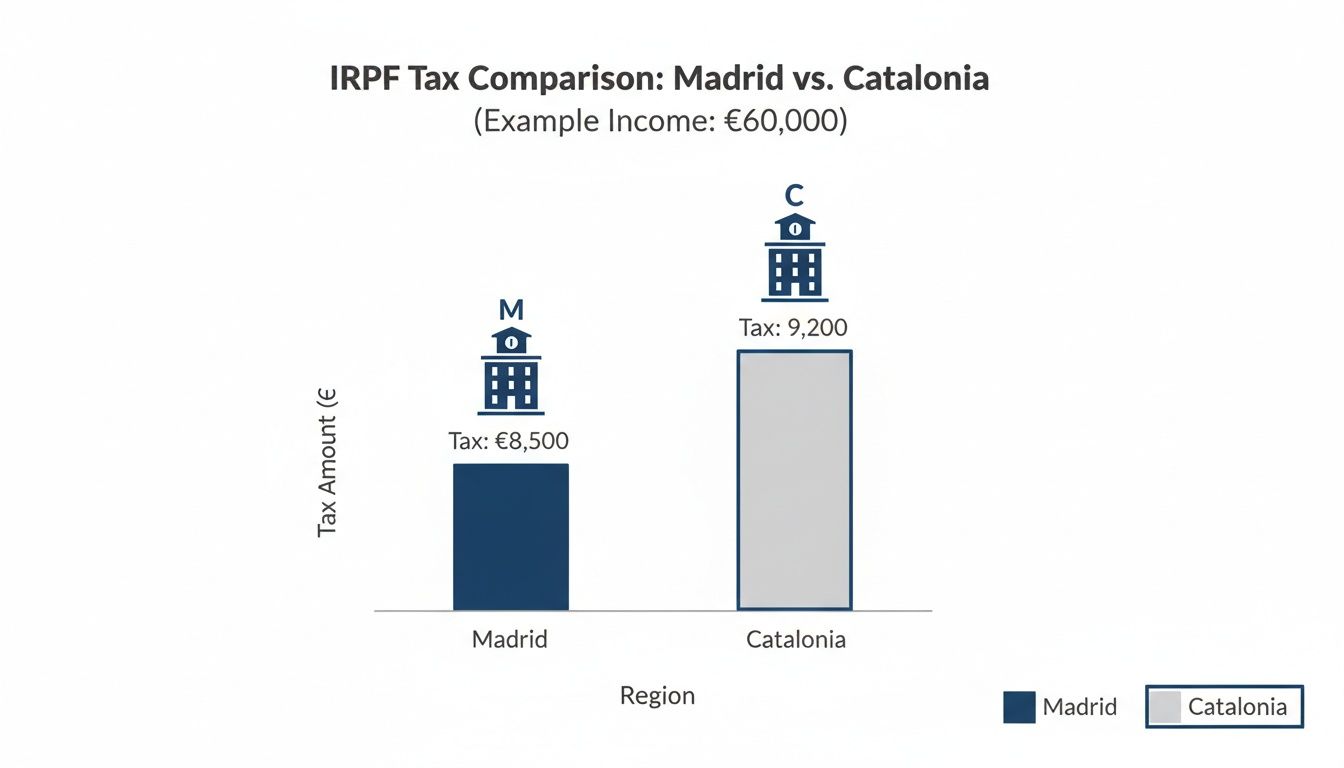

Beyond the standard minimums, a world of specific deductions opens up based on your investments, work, and life choices. These require paperwork, but the savings are worth the effort.

The infographic below shows how regional deductions can impact your final tax bill. A €60,000 salary doesn't feel the same in every city.

As you can see, the same €60,000 income results in a lower tax liability in Madrid than in Catalonia. This isn't a mistake; it's the direct result of different regional tax policies.

Here are a few of the most common—and often missed—deductions our clients use:

Mortgage Interest on Primary Residence: This is a legacy deduction. You can only claim it if you bought your home before 1st January 2013. If that’s you, you can deduct up to 15% of your mortgage payments on a maximum of €9,040 per year.

Pension Plan Contributions: Putting money into a qualifying private pension plan in Spain (or another EU country) is a smart move. It's also deductible, up to a maximum of €1,500 per year.

Charitable Donations: Giving to registered charities pays back. You can deduct 80% of the first €250 you donate and 40% of anything you give above that amount.

Work-from-Home Expenses for Autónomos: If you're a registered freelancer (autónomo) and work from home, a portion of your utility bills (water, electricity, internet) is deductible. The standard calculation is 30% of the proportion of your home you use just for work.

Each deduction has its own rules. In our experience, many expats miss out because they don't know these deductions exist or can't navigate the documentation.

If you want to make sure you're claiming every cent you're entitled to, contact us for personalized advice. We'll review your situation and build a strategy to make your IRPF declaration as efficient as possible.

Special Tax Regimes: The Beckham Law and Non-Resident Rules

Beyond the standard progressive IRPF, Spain has special tax regimes that are huge draws for foreigners. These aren't just minor tweaks; they can completely change how much tax you pay.

Understanding the difference between being a standard tax resident, a Beckham Law beneficiary, or a non-resident is the first step to making smart financial decisions in Spain.

The Beckham Law: A Flat-Tax Game Changer

One of the most famous options is the Special Regime for Inpatriates, better known as the "Beckham Law." It was designed to pull high-skilled foreign talent to Spain. The core idea is simple: instead of taxing you on your worldwide income at climbing rates, it treats you more like a non-resident for your first six years here.

The main attraction is the flat tax rate. For the year you arrive and the next five years, you pay a flat 24% tax on your Spanish employment income up to €600,000. Anything you earn from your Spanish job above that gets hit with a 47% rate. For high earners who would otherwise be pushed into Spain's top IRPF brackets—which can top 50% in some regions—the savings are massive.

The Beckham Law lets you opt out of the progressive IRPF system. It taxes your Spanish income at a predictable flat rate, and your foreign income (like capital gains or rental income from back home) generally stays outside of Spain’s tax net.

But it's not a free-for-all. In our experience, the eligibility rules are strict. To get in, you have to meet a few key conditions:

- You can't have been a tax resident in Spain for the five years before you move.

- Your move to Spain must be because of a Spanish employment contract.

- The work has to be physically done in Spain.

For a full breakdown of the requirements and the application process, check out our detailed guide on who actually qualifies for the Beckham Law. It’s a powerful tool, but you have to apply correctly and within six months of starting your job.

Non-Resident Income Tax (IRNR)

What happens if you aren't a tax resident and the Beckham Law doesn't apply, but you're still earning money in Spain? That’s where the Impuesto sobre la Renta de No Residentes (IRNR) comes in. This is a separate tax system for people who don't meet the residency criteria but have Spanish income.

Unlike the IRPF's sliding scale, IRNR uses flat rates. The general rate for EU/EEA residents is 19%. For everyone else, it’s 24%. This tax typically applies to a few common situations:

- Rental Income: You own a flat in Spain and rent it out.

- Capital Gains: You sell a Spanish asset, like that flat.

- Pensions: In some cases, if your pension is paid from a Spanish source.

For expats or investors with property in Spain, knowing how this works is critical. A good general guide for understanding property tax implications can give you the bigger picture of your financial obligations.

Figuring out which of these categories you fall into—standard resident, Beckham Law beneficiary, or non-resident—is fundamental. Each path comes with its own rules and benefits.

If you’re not sure which box you fit in or which regime makes the most financial sense for you, contact us for personalized advice. We'll walk you through the options and help you land on the most efficient tax strategy.

How to File Your IRPF: The Annual Declaration

Knowing what IRPF is gets you halfway there. Navigating the annual filing process—the declaración de la renta—is the other half. Each year, tax residents in Spain must report their income and settle their accounts with the Agencia Tributaria (the Spanish Tax Agency). The main tool for this is a form known as Modelo 100.

This yearly ritual runs on a strict schedule. The tax campaign usually opens in early April and closes firmly on the 30th of June. Missing that deadline is a surefire way to attract penalties.

Who Is Required to File a Tax Return

Not every resident is legally required to file, but in our experience, the thresholds are low enough that most working expats must. You absolutely must file an IRPF declaration if you meet any of these conditions:

- Your yearly income from a single employer tops €22,000.

- Your yearly income from two or more employers is over €15,000, provided the second (and any subsequent) employer paid you more than €1,500 combined.

- You have other income sources, like capital gains or rental income, that exceed specific, lower thresholds.

That multiple-employer rule catches a lot of people off guard. If you switched jobs mid-year or had a small side project, you’re almost certainly required to file, even if your total earnings were under €22,000.

Using the Renta WEB Portal and the Borrador

The Agencia Tributaria has made things easier with its online portal, Renta WEB. Through this system, you can access a pre-filled draft of your tax return, called the borrador. The tax office populates this draft with information it already has from your employer and bank.

But here’s the critical part: convenient doesn’t mean complete. It's a mistake to just accept the borrador as is.

The draft declaration is a starting point, not the final word. It often omits key deductions, personal allowances for children, or details about foreign income that the tax office doesn't automatically know about. Blindly submitting it can cost you money.

You must review and correct the draft. This means double-checking that every income source is listed and, crucially, adding every deduction you are entitled to. This is precisely where professional help pays for itself. We navigate the maze of the Spanish tax system for our clients, from straightforward filings to complex scenarios. Learn more about our income tax filing services in Spain.

Consequences of Late Filing

Those deadlines aren’t suggestions. Filing your IRPF late—or forgetting—triggers automatic penalties. The fine depends on whether you file voluntarily before they contact you and whether you owe money or are due a refund.

- Late filing (voluntary): If you realize your mistake and file late on your own, the penalty is a surcharge between 1% and 15% of the tax due, plus late-payment interest.

- Late filing (after notification): If the tax agency has to come looking for you, the penalties get serious, starting at 50% of the tax you owe and climbing higher.

Wrestling with the annual tax declaration can be overwhelming, especially in a foreign system. Our team handles the entire process for clients across Spain, ensuring your Modelo 100 is filed accurately, on time, and optimized to your benefit.

Common Questions About IRPF

We get a lot of questions about how IRPF works. Here are quick, practical answers to the ones we hear most often from our clients.

Can I Avoid IRPF if I'm Paid by a Foreign Company?

No. This is one of the most common—and expensive—misunderstandings we see. If you live in Spain long enough to be a tax resident (usually by crossing the 183-day mark), your worldwide income is on the table.

It doesn’t matter if your salary comes from a company in London or lands in a bank account in Delaware. If you live here, Spain expects its share. It must be declared.

Is My Pension From Back Home Taxable in Spain?

Yes, for most tax residents, it is. The vast majority of double taxation treaties give the country where you reside the right to tax your pension.

This means that a pension you receive from the UK, the US, or Germany is considered regular income here. You’ll need to include it on your annual IRPF declaration.

Do I Owe Spanish Tax on Worldwide Capital Gains?

Absolutely. As a Spanish tax resident, you are taxed on gains from all your assets, no matter where they are located.

Selling a property in another country, cashing out stocks on a foreign exchange, or liquidating crypto assets—it all creates a taxable event in Spain. These gains are taxed at progressive rates, starting at 19% and going up to 28%.

What Is This Article 7p Exemption I've Heard About?

Article 7p is a powerful tax break for Spanish residents who travel for work. It allows you to exempt up to €60,100 of the salary you earn while physically working outside of Spain, as long as that work benefits a non-Spanish company.

The rules are incredibly strict and require meticulous records. For executives and consultants who travel often, the savings are substantial. This is a specialized area where getting professional advice is non-negotiable.

Navigating Spanish tax law isn't just about paying what you owe; it's about not paying more than you have to. If you're unsure how these rules affect your specific situation, our team can build a clear, tax-efficient strategy for you. Book a consultation with us for personalised advice.