If you're a tax resident in Spain, there’s a form you can't ignore: Modelo 720. It's the Spanish government’s way of asking, "What assets do you have outside of Spain?"

This isn't a tax bill. It's a declaration. You're telling the Spanish Tax Agency (Agencia Tributaria) about your foreign bank accounts, investments, and real estate. But getting it wrong, or not filing at all, comes with serious penalties.

What Is Modelo 720 and Do You Need to File?

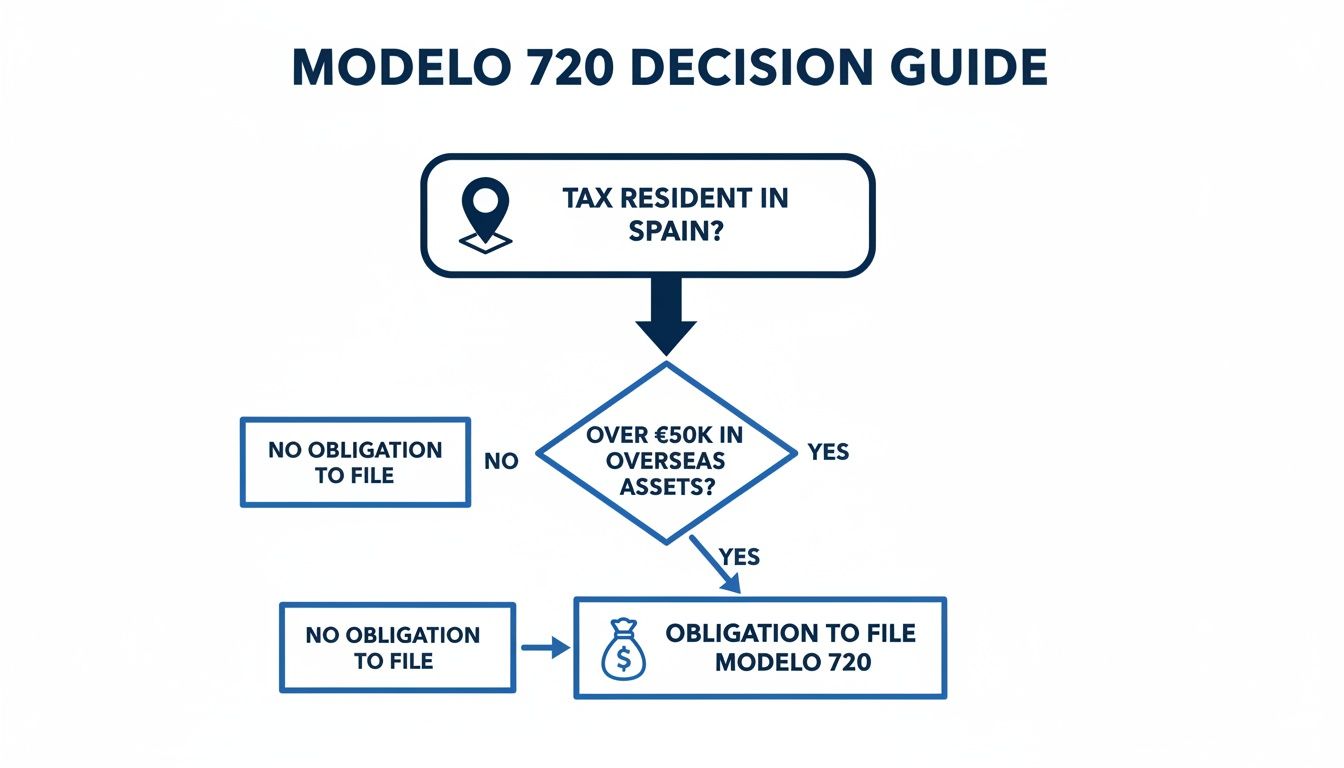

So, who exactly needs to worry about this? The rule is simple: if you are a tax resident in Spain and the value of your assets in any single category abroad exceeds €50,000, you must file.

Tax residency is usually determined by spending more than 183 days a year in Spain, or if your primary economic interests are based here. It catches many expats, retirees, and digital nomads who have made Spain their home but maintain financial ties abroad. For a deeper look into the form itself, you can read our detailed guide on what is Modelo 720.

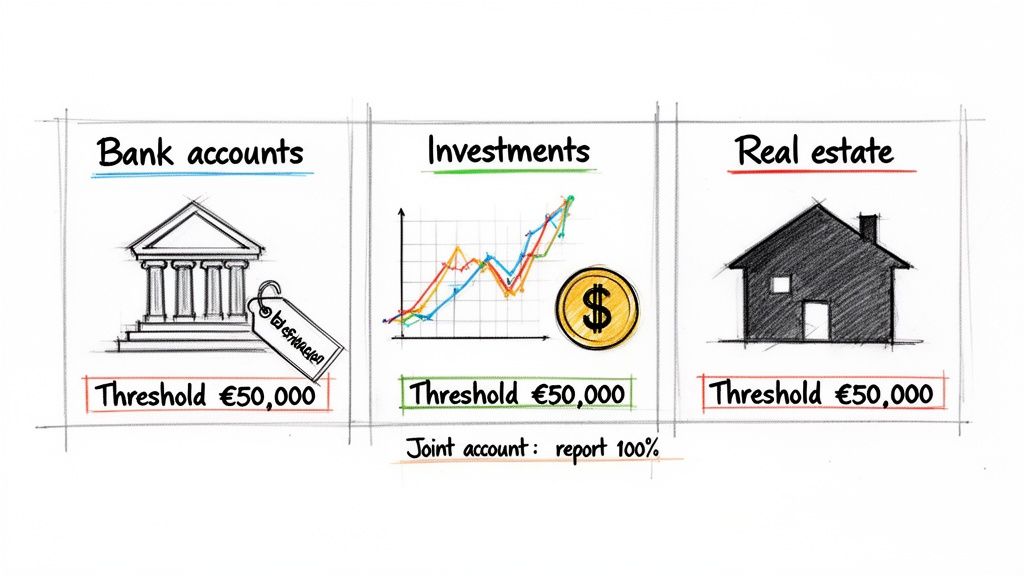

The declaration breaks down your foreign assets into three distinct blocks:

- Block 1: Bank accounts held in financial institutions abroad.

- Block 2: Investments, securities, life insurance policies, and income managed or generated overseas.

- Block 3: Real estate and rights over property located outside of Spain.

The €50,000 threshold is the magic number, and it applies to each block separately. This is a critical detail. You don't add the blocks together.

Let’s say you have €40,000 in a UK bank account, €30,000 in US stocks, and a small apartment in France worth €45,000. In this case, you don't need to file Modelo 720 because no single category tops the €50,000 limit. But if that UK bank account had €50,001, you'd have to declare the entire balance for that block.

This flowchart gives you a quick visual guide to see if the obligation applies to you.

As you can see, it boils down to two questions: Are you a Spanish tax resident? And do your foreign assets in any of the three categories exceed €50,000?

The Modelo 720 Filing Quick Check

Use this table for a quick self-assessment. If you answer "Yes" to both of the main criteria for any asset block, you likely have a filing obligation.

| Criteria | Requirement | Do You Meet This? (Yes/No) |

|---|---|---|

| Residency Status | Are you considered a tax resident in Spain for the relevant year? | |

| Asset Block 1: Accounts | Do your total balances in foreign bank/financial accounts exceed €50,000? | |

| Asset Block 2: Investments | Does the total value of your foreign investments, insurance, and annuities exceed €50,000? | |

| Asset Block 3: Real Estate | Does the acquisition value of your foreign real estate exceed €50,000? |

This is just a starting point. The specifics of valuation dates and what counts within each block can get complicated, but it’s a good first check.

Is Modelo 720 a Tax?

No. Let’s be perfectly clear on this point, as it’s the most common question we get. Modelo 720 is purely an informational declaration. You don’t pay tax when you file this form.

Its purpose is to provide the Agencia Tributaria with a clear picture of your global assets. They use this information to cross-reference your other tax filings, like your annual income tax (Impuesto sobre la Renta de las Personas Físicas, or IRPF) and Wealth Tax returns. If you declare a rental property in Germany on Modelo 720, they’ll expect to see that rental income show up on your IRPF.

Think of it as the foundation of your tax compliance in Spain. Getting it right ensures everything else builds on a solid, transparent base. If you’re even slightly unsure whether your situation requires a declaration, it’s far better to get clear advice than to risk the consequences.

Who Qualifies as a Spanish Tax Resident

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

The duty to file Modelo 720 comes down to one question: are you a Spanish tax resident? Many expats think it’s just about counting days, but the Agencia Tributaria (Spain’s tax agency) has a more sophisticated approach. They use a few different tests, and you only need to meet one of them.

The most famous test is the 183-day rule. If you spend more than 183 days physically inside Spain during a calendar year, you’re automatically a tax resident. The days don’t need to be consecutive, and short trips abroad often won’t save you unless you can prove tax residency somewhere else.

The Centre of Economic Interests Test

Spain also looks at where your money is made. This is your centre of economic interests. If the core of your professional life or business operations is in Spain, the tax authorities will consider you a resident, no matter how many days you were here.

For instance, say you’re a remote worker living in Valencia. Even with frequent international travel, if your main clients are Spanish and your income is generated here, your economic centre is in Spain. We see this often with digital nomads and entrepreneurs who assume their travel exempts them. It doesn’t.

The Centre of Vital Interests Test

Then there’s the centre of vital interests, which is about where your life happens. This test is personal, focusing on your family and social roots. The law presumes you’re a resident if your spouse (unless legally separated) or dependent minor children live in Spain.

This is a powerful assumption. If your kids go to a Spanish school and your partner lives here, arguing that your vital interests are elsewhere is an uphill battle, even if your work keeps you on the road. You can learn more about the specifics in our complete guide to Spanish tax residency.

The burden of proof to demonstrate otherwise falls on you.

What About the Beckham Law?

This is an area where many people get mixed messages. Taxpayers who are applying the special impatriate regime under article 93, widely known as the Beckham Law, should not be analysed in the same way as ordinary Spanish tax residents for Modelo 720 purposes.

According to current AEAT guidance, taxpayers covered by the special impatriate regime do not file Modelo 720 while they remain under that regime.

That means the normal foreign-asset reporting analysis in this article is aimed at standard Spanish tax residents. If you are under the Beckham Law, your filing position should be checked separately before assuming that Modelo 720 applies to you.

Who Else Must File?

The filing requirement isn’t just for individuals. Modelo 720 obligations also apply to certain legal structures and entities based in Spain.

- Spanish-resident companies and other legal persons.

- Permanent establishments in Spain that belong to non-resident individuals or companies.

- Other entities like inheritances awaiting distribution (herencias yacentes) that are considered Spanish-based.

Getting your tax residency status right is the absolute first step. A mistake here can be incredibly expensive.

Asset Categories and How to Report Them

The Modelo 720 organises foreign assets into three distinct “blocks.” Getting this right is everything. The single most important rule is that the €50,000 threshold applies to each block separately. You don’t add them together.

In our experience, this is a point of huge relief for many new residents we advise. If you don’t cross the €50,000 line in any single category, you don’t have to file. For instance, having €40,000 in a US bank account, €45,000 in UK stocks, and a small property stake in France worth €49,000 means you have no filing obligation.

Block 1: Bank Accounts

This is the most straightforward category. It covers any accounts held in financial institutions outside of Spain.

- Checking and current accounts

- Savings accounts

- Fixed-term deposit accounts

You must file if the total value of all accounts in this block tops €50,000. The tax office looks at two figures: the balance on December 31st and the average balance over the final quarter. If either one exceeds the threshold, you must declare all accounts in the block.

A detail many people miss: being an authorised signatory or beneficiary on an account, even if it isn’t “yours,” can trigger a reporting duty. The Spanish Tax Agency wants to know about any foreign accounts you can control or benefit from.

Joint accounts are a common tripwire. If you and your spouse hold a joint account abroad with a balance of €80,000, you both have to file a Modelo 720. On your individual forms, you’ll each report the full €80,000 balance and then clarify your ownership percentage (e.g., 50%).

Block 2: Securities and Investments

This is the broadest and often the trickiest block. It lumps together a wide range of financial assets that are deposited, managed, or held abroad. The €50,000 threshold applies here, too, based on the total value on December 31st.

This block includes:

- Stocks, shares, and other equity in foreign companies.

- Investment funds, whether held directly or through a foreign platform.

- Life insurance policies and annuities from non-Spanish providers.

- Certain pension plans, which can be a complex area depending on the plan’s structure and country of origin.

Let’s use a practical example. Say you’re a professional who moved to Spain on a Digital Nomad Visa. You have a UK pension pot worth €60,000 and some shares in a US tech company valued at €55,000. If those assets fall within this block, they can trigger a Modelo 720 filing because the relevant category exceeds the €50,000 threshold.

Block 3: Real Estate

The final block covers real estate you own outside of Spain. This applies to direct ownership of property as well as certain rights over foreign property, such as timeshares.

Here’s the critical difference: the €50,000 threshold is based on the acquisition value of the property, not what it’s worth today. If you bought a flat in London 20 years ago for €40,000, it doesn’t matter that it’s now worth €200,000. On its own, it doesn’t require reporting.

However, you must add up the acquisition costs of all foreign properties you own. If you bought one flat for €30,000 and another for €35,000, your total acquisition cost is €65,000. This pushes you over the threshold, and you must declare both properties.

Valuations and Exchange Rates

For every asset, you must convert its value into Euros. The Spanish Tax Agency is very specific about this. You must use the official exchange rate published by the Bank of Spain as of December 31st of the tax year. Don’t just grab a rate from Google; using the official one is mandatory.

Getting these categories and valuations right is fundamental. If you’re managing assets across different countries, the process can feel overwhelming. Contact us for personalised advice. We’ll help you classify each asset correctly and make sure your declaration is accurate.

How to File Your Modelo 720 Declaration

Knowing if you need to file Modelo 720 is half the battle. The other half is getting it done. The process is strict, entirely digital, and can trip up even the most organised new resident.

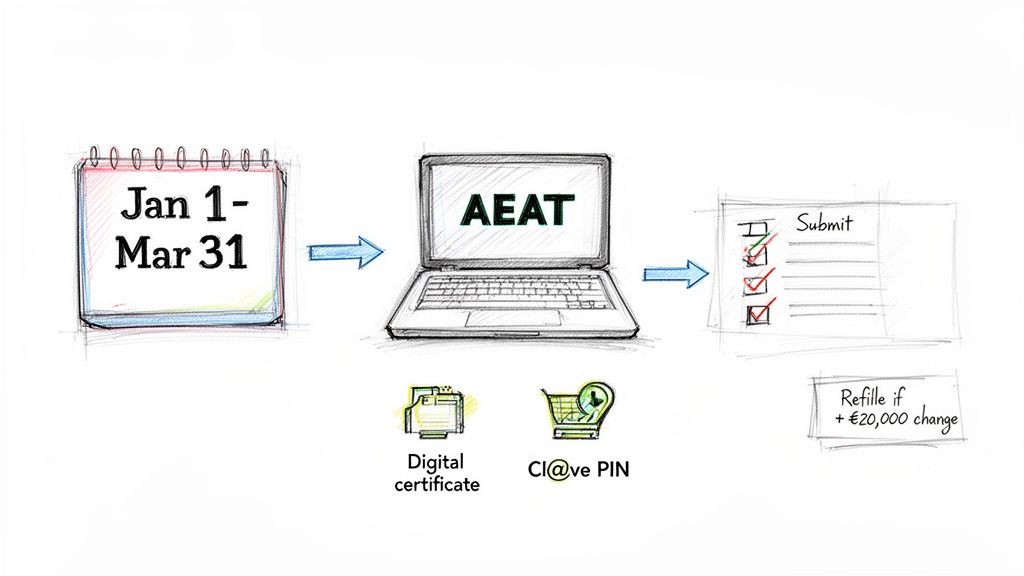

The filing window is non-negotiable. You must submit your declaration between January 1st and March 31st each year. This filing reports the assets you owned on the last day of the previous year.

So, for assets held on December 31st, 2025, your deadline is March 31st, 2026. Miss it, and you face penalties. Put it on your calendar.

How to Submit Your Declaration

Modelo 720 is filed online. You can’t print a form and mail it in. The only way is through the official website of the Spanish Tax Agency, the Agencia Tributaria (AEAT).

To get through the digital door, you’ll need a Spanish digital ID. This usually means one of two things:

- Digital Certificate (Certificado Digital): This is the gold standard for official online business in Spain. It’s a file you install on your computer that securely verifies your identity for everything from taxes to social security.

- Cl@ve PIN System: A more mobile-friendly option that sends temporary access codes to your phone. It’s often quicker to set up but can be less versatile for more complex filings.

In our experience, getting these credentials is the single biggest hurdle for most expats. The process involves online applications and in-person appointments, and it isn’t always straightforward. We advise clients to start this process months before the March deadline to avoid a last-minute scramble.

Do I Have to File Every Single Year?

This is the most common question we get, and the answer is a relief for many. No, you do not have to file Modelo 720 every single year after your first declaration.

You only need to file again if your situation changes in one of three specific ways:

- Your assets grew: The value of a previously reported asset category (like bank accounts) has increased by more than €20,000.

- You sold or closed something: You’ve sold a foreign property, closed a bank account, or otherwise disposed of an asset you reported before.

- You acquired something new: You bought a new reportable asset, even if it doesn’t push that category’s total value up by €20,000.

Understanding these rules is key. It means you only do the administrative work when absolutely necessary.

Navigating the AEAT portal and getting your digital ID sorted can be a headache. If you’re wrestling with the process or just want to make sure it’s done right, we can guide you through every step.

Common Mistakes and Penalties to Avoid

The Most Frequent Errors We See

In our experience, nearly all Modelo 720 problems come from a handful of recurring oversights. Knowing what they are is your best defence.

Here are the specific tripwires we see most often:

- Forgetting joint accounts: If you and your spouse hold a joint account abroad with over €50,000, you both have to file a Modelo 720. Each of you declares the full balance and notes your ownership percentage.

- Using the wrong exchange rate: You can’t just pull a rate from your favourite currency app. The Hacienda requires you to use the official exchange rate published by the Bank of Spain for December 31st of the reporting year.

- Miscalculating thresholds: The €50,000 threshold applies to each of the three asset categories separately. You don’t add them all together to see if you qualify.

- Ignoring the €20,000 growth rule: This is a big one. You must re-file if the total value of a previously declared asset group grows by more than €20,000. Many expats file correctly the first year and completely forget this rule in subsequent years.

- Ignoring signatory powers: You don’t have to “own” the money. Just being an authorised signatory on someone else’s foreign account can trigger your own reporting obligation.

Understanding the Current Penalty System

You may have heard horror stories about the old Modelo 720 penalties. That regime was rightly struck down by the EU’s Court of Justice in 2022 for being disproportionate.

But “less harsh” doesn’t mean “no penalties”. The fines today are still serious and are governed by Spain’s general tax law, the Ley General Tributaria.

The current standard penalty for filing late or with errors is €20 for each piece of missing or inaccurate data. This carries a minimum fine of €300 and a maximum of €20,000.

Think about it. Forgetting to declare a single foreign bank account means multiple missing data points: the bank’s name, the account number, the balance. Those €20 fines can stack up quickly.

The Best Strategy Is Proactive Compliance

What if you’ve missed a deadline or just discovered you should have filed years ago? Don’t panic, and definitely don’t bury your head in the sand. The smartest move is always to file voluntarily before the tax office contacts you.

Filing proactively shows good faith and can slash penalties, often by 50% or more, compared to what you’d face if the Agencia Tributaria finds the error first. With automatic information exchange agreements between countries, it’s only a matter of when, not if.

Getting this right isn’t just about avoiding a fine; it’s about securing your peace of mind. If you’re unsure about your obligations or have found a past mistake, contact us for personalised advice. We can help you fix the issue and make sure your finances are fully compliant.

How Modelo 720 Impacts Your Other Spanish Taxes

It’s a common misunderstanding. New residents often see the modelo tributario 720 and assume it’s another tax bill. Let’s be perfectly clear: it’s not. You don’t pay a single euro when you file this form.

Think of it as the Spanish Tax Agency’s (Agencia Tributaria) information-gathering tool. Its sole purpose is to give them a complete, transparent view of the assets you hold outside of Spain. But this information doesn’t just sit in a file somewhere. The Hacienda uses your Modelo 720 data to check your other tax filings.

The Connection to Your Income Tax (IRPF)

The most direct link is to your annual income tax return, known as the Renta or Modelo 100 (IRPF). Any asset you list on Modelo 720 that generates income must have those earnings reported on your IRPF. The tax office’s systems are built to automatically flag inconsistencies.

For example, if you declare a rental property in France on your Modelo 720, the tax office absolutely expects to see that rental income on your Modelo 100. If you declare a foreign investment portfolio, they’ll be looking for dividends and capital gains. A mismatch is a bright red flag that often triggers a tax audit.

Impact on the Spanish Wealth Tax

The data from Modelo 720 also feeds directly into their calculations for Spain’s Wealth Tax, or Modelo 714. This tax is applied to your net worldwide assets. The threshold varies by region but generally kicks in around €700,000, plus a €300,000 exemption for your primary home in Spain.

When you submit Modelo 720, you’re essentially handing the tax authorities an itemised list of your foreign assets. They will add this to the value of your Spanish assets (like property) to calculate your total net worth. If that number crosses the regional threshold, you are legally obligated to file and pay the Wealth Tax. For a broader look at tax obligations, see our guide on taxes for expats in Spain.

Different tax regimes can change how foreign income and foreign assets are treated, so your Modelo 720 position should always be checked together with your wider Spanish tax status.

Failing to declare assets on Modelo 720 and then, as a result, not filing a required Wealth Tax return creates a serious problem. The tax office can reclassify those hidden assets as “unjustified capital gains” and tax them at your highest marginal income tax rate, on top of severe penalties.

Keeping all your tax filings consistent isn’t just good practice—it’s your best defence against audits and fines. If you’re managing assets both in and out of Spain, getting a clear, unified view of your obligations is critical.

Common Questions About Modelo 720

What if I Missed the Deadline?

You missed the 31st March deadline. Don’t panic, but don’t hide. Waiting for the Agencia Tributaria (the Spanish tax office) to find you is the worst possible strategy. And they will find you—automatic information exchange between countries makes it inevitable.

The best move is to file a voluntary late declaration. Taking this step shows good faith and almost always reduces the fines, often by 50% or more. This is a much better outcome than facing the full penalties that arrive after an official notice lands on your doorstep.

How Do We Declare a Joint Account?

This trips up a lot of people. Imagine you and your partner have a joint account in the UK with a balance of €80,000. The reporting rule is individual. You must both file a Modelo 720.

On each of your separate forms, you have to do two things:

- Declare the entire account balance—€80,000.

- State your ownership percentage, for example, 50%.

You can’t just split the balance and report €40,000 each. That’s an incorrect filing and can trigger fines for providing inaccurate information.

Do I Report Crypto on Modelo 720?

Not anymore. This is a recent and important change. For years, crypto sat in a grey area, but Spain now has a specific form just for virtual assets held abroad.

Cryptocurrency is now declared on a completely separate form: Modelo 721. This form has its own €50,000 threshold and the same filing window, from 1st January to 31st March.

This is an independent obligation. You might not need to file a Modelo 720 for your bank accounts or property, but you could still be required to file a Modelo 721 for your crypto. The two are no longer reported together.

If these questions sound familiar, or if your own situation feels complicated, getting the declaration right is critical. We can provide clear advice to ensure your filing is correct and complete. Contact us for personalised advice and navigate the Modelo 720 with confidence.