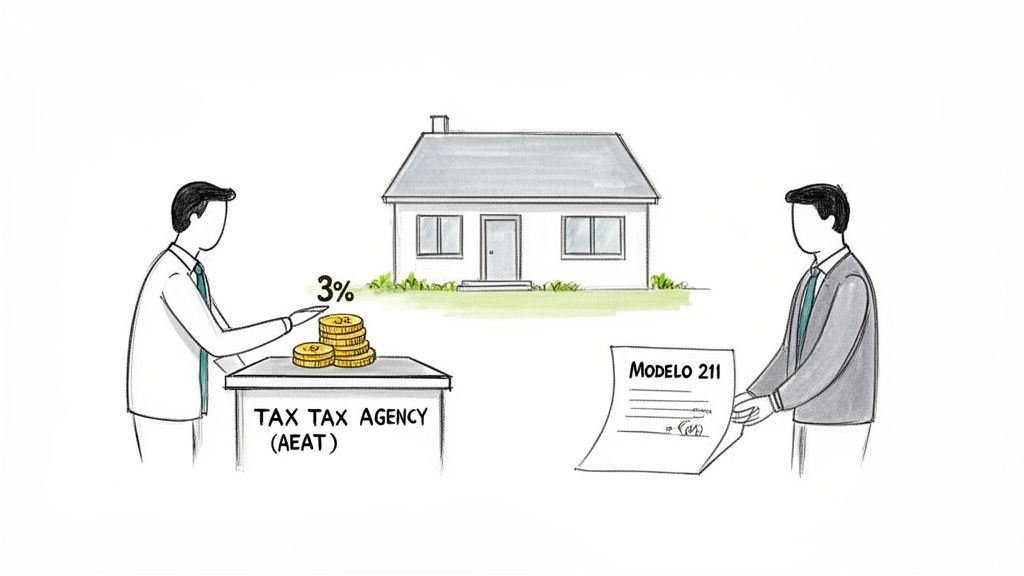

If you’re buying a property in Spain from a non-resident, you’ll quickly run into the term AEAT Modelo 211. This isn’t a tax you owe. Instead, it’s a form the buyer uses to handle a 3% retention from the sale price, which you pay directly to the Spanish Tax Agency (AEAT).

Think of it as a security deposit against the seller’s future tax bill.

What Is Modelo 211 and Why Does It Matter?

When a non-resident sells Spanish property, the law obligates you, the buyer, to withhold 3% of the total purchase price. You then submit this amount to the AEAT using the Modelo 211 form. It’s a formal receipt for a mandatory down payment on the seller’s behalf.

This entire process is a safety net for the Spanish government. It ensures they get an advance on the seller’s potential capital gains tax, preventing sellers from leaving the country without settling their tax obligations.

If this 3% turns out to be higher than the seller’s final tax liability, the seller can request the difference back through the correct Modelo 210 filing. The processing time is not fixed and depends on how the AEAT reviews the file and the documentation provided.

The Buyer’s Role vs. The Seller’s Role

This is often where confusion arises. It is therefore important to clearly define the respective responsibilities:

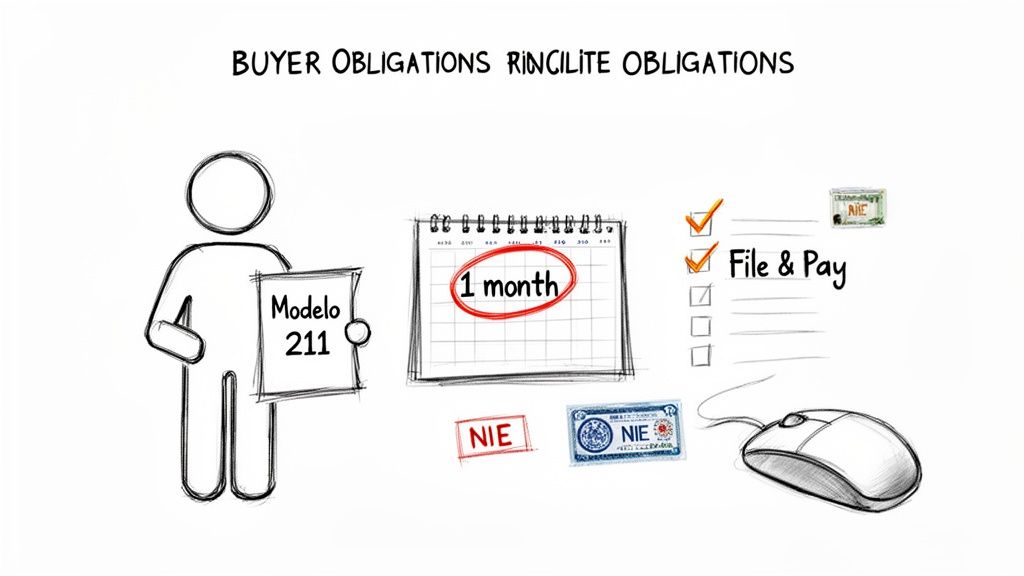

- The Buyer: Your job is to withhold the 3%, file Modelo 211, and pay that retained amount to the tax authorities. You have exactly one month from the date of the sale to do this.

- The Seller: Later on, the seller must file a different form, Modelo 210, to declare their final capital gain or loss. The 3% you paid for them is then credited against whatever tax they owe.

The buyer pays the 3% retention using Modelo 211. The seller settles their final tax account using Modelo 210. Getting this right is fundamental to a smooth transaction.

This division of duties is central to how non-resident property tax works in Spain. One mistake can create serious problems for both you and the seller.

Modelo 211 vs. Modelo 210 at a Glance

It’s easy to mix these two forms up. Both are for non-resident property sales, but they serve completely different functions for different people. This table breaks it down.

| Feature | Modelo 211 (Retention) | Modelo 210 (Tax Declaration) |

|---|---|---|

| Who Files It? | The buyer of the property. | The non-resident seller of the property. |

| What Is It For? | To pay the 3% retention on the seller's behalf. | To declare the capital gain or loss from the sale. |

| When Is It Filed? | Within one month of the property sale. | Within three months following the end of the one-month retention period. |

| Primary Purpose | A down payment to secure the seller's future tax. | The final calculation and settlement of the seller's tax bill. |

Understanding this table is the first step. The buyer’s duty is with Modelo 211; the seller’s is with Modelo 210. They are two sides of the same coin, but you must know which side is yours.

For a broader look at the taxes involved, our guide on Spanish property tax for non-residents provides more context. Properly managing these forms from the outset is the best way to avoid future headaches and penalties.

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

Your Obligations for Filing Modelo 211

Let’s cut straight to the most important point for any buyer: the legal duty to file AEAT Modelo 211 and pay the 3% retention falls squarely on you. It doesn’t matter if you’re a Spanish resident or a foreigner yourself. If you buy a Spanish property from a non-resident seller, this responsibility is yours.

If you fail to file and pay, the Spanish Tax Agency (AEAT) can hold you liable under the applicable regime. The property itself is also affected for the lower of the retention or payment on account and the corresponding tax debt, with the registry note that applies in law.

The Strict One-Month Deadline

You have a very tight window. The deadline to file Modelo 211 and pay the retention is exactly one month from the date you sign the public deed of sale, the escritura pública. This is not a flexible timeframe.

So, if you sign the deed at the notary on March 15th, your deadline to submit the form and pay the 3% is April 15th. Missing this date triggers penalties and complicates things for the seller, who needs your filing receipt to settle their own capital gains tax.

The buyer is legally responsible for withholding the 3%, filing Modelo 211, and paying the tax authority within one month of the sale. This is not the seller’s responsibility.

Who Is Obligated to File

The obligation is on the acquirer—the buyer. This is a critical distinction. It applies whether you are buying as an individual, a couple, or a company. If there are multiple buyers on the deed, you are all jointly responsible for making sure the retention is paid.

The whole process can feel overwhelming, especially for foreign buyers unfamiliar with Spanish tax procedures. This is why most of our international clients appoint a fiscal representative. It ensures the calculation is correct, the form is filed properly, and the deadline is met without any last-minute stress.

Getting these details right is fundamental to a clean property purchase. Our team handles every aspect of non-resident tax in Spain and can manage the Modelo 211 filing for you. Contact us for straightforward advice to ensure your purchase is compliant from day one.

How to File the Modelo 211

Alright, you’ve bought the property. Your next job as the buyer is to file the AEAT Modelo 211 and pay the 3% retention you withheld from the seller. This falls squarely on your shoulders.

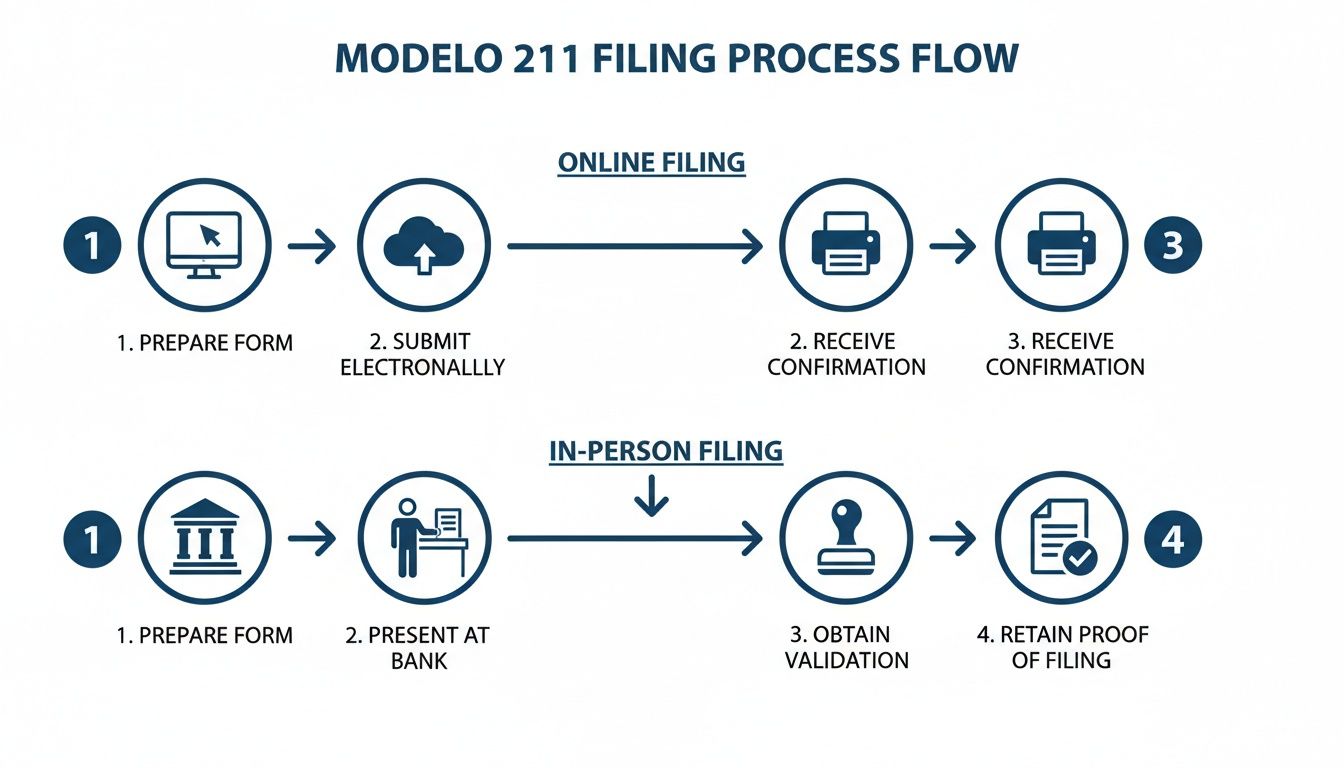

You effectively have three filing routes to consider: ordinary electronic filing, electronic filing with payment by transfer in the cases allowed by AEAT, and the pre-declaration route for payment through a collaborating bank.

If you already have a Spanish digital certificate or Cl@ve, the electronic route is usually the fastest. In cross-border transactions, the transfer-payment route may also be relevant depending on how the payment is structured. Where neither option is practical, the pre-declaration route through a collaborating bank remains available. A fiscal representative can also handle the filing for you and keep the timeline under control.

The Online Filing Method

Filing online is the most direct way to get this done. You’ll need your Spanish digital credentials ready.

- Find the Form: Go to the AEAT website and pull up Modelo 211.

- Fill It Out: You need to enter all the details from the sale perfectly: your information, the non-resident seller’s details (especially their NIE), the property information, the full sale price, and the exact 3% you withheld.

- Submit and Pay: Use your digital certificate or Cl@ve to sign and submit the form. The system will let you authorise a direct debit from your Spanish bank account to pay the retention. You’ll get an official receipt immediately, which is your proof of compliance.

The instant confirmation is great for peace of mind and your records.

The In-Person Filing Method

No digital certificate does not mean you are blocked. The usual paper route starts by generating a pre-declaration on the AEAT website.

The system produces the corresponding copies for the buyer, the collaborating bank, and the non-resident seller. From there, the payment is made through the collaborating entity and the stamped or validated documentation must be kept carefully so the seller can later regularise the transaction through Modelo 210.

The key point is that the paper route follows the official pre-declaration and bank-copy workflow. It is not safely described as simply taking a stamped form to the tax office at the end.

If you are unsure which filing route applies, it is better to confirm it before the deadline rather than improvise once the month is already running.

Common Errors to Avoid

We see the same mistakes trip people up time and again. Getting these wrong can cause serious delays and trigger penalties, so pay close attention.

- Incorrect NIE Numbers: A single typo in the buyer’s or seller’s NIE can get the entire filing rejected. Double-check everything.

- Miscalculating the 3%: The retention must be exactly 3% of the full purchase price listed in the escritura (deed). Not a cent more or less. Any other figure will be flagged.

- Missing the Deadline: You have exactly one month from the signing date. The AEAT is not flexible on this. Filing late means automatic fines and interest.

Getting the AEAT Modelo 211 filed correctly is a non-negotiable step in your property purchase. If you have any doubts or simply want an expert to handle it, we’re here to help. Contact us for personalised advice.

How the 3% Retention Affects Your Capital Gains Tax

Alright, let’s shift focus back to you, the non-resident seller. The buyer has filed Modelo 211 and paid 3% of the sale price to the tax office. What does that mean for you?

Think of that 3% retention not as a separate tax, but as a down payment on your final capital gains bill. It’s an advance payment made on your behalf.

Once the buyer has done their part, the ball is in your court. Your next move is to file a different form, Modelo 210, to officially declare the profit or loss from your sale. This is where you settle up with the tax authorities, squaring your actual liability against the 3% they’re already holding.

Calculating Your Capital Gains

Figuring out your final tax isn’t as simple as sale price minus purchase price. The tax office wants a more detailed calculation. You start with the final sale price, then subtract the original purchase price and all the associated costs.

These deductible expenses are critical for lowering your tax bill. They can include:

- The original transfer tax (ITP) or VAT you paid when you first bought the property.

- Notary and Land Registry fees from your initial purchase.

- Legal and real estate agent fees from both buying and selling.

- The cost of major renovations or improvements, as long as you have official invoices (facturas).

Keeping meticulous records of these costs is essential. Every euro you can legitimately deduct is a euro off your taxable gain. For a complete breakdown, our guide on Capital Gains Tax in Spain covers this in detail.

Spain’s capital gains tax rates are progressive. The first €6,000 of profit is taxed at 19%. The next slice, from €6,001 to €50,000, is taxed at 21%. The rates continue to climb, reaching up to 30% for gains over €300,000. Getting the calculation right is key.

This flowchart maps out the process for sellers after the Modelo 211 retention has been paid.

As you can see, filing your own tax return can lead to one of two outcomes: paying more tax or getting a refund.

Two Possible Outcomes for the Seller

After you file your Modelo 210 and the exact tax is calculated, you’ll find yourself in one of two situations.

- Tax Owed is More Than the 3% Retention: If your final capital gains tax is higher than the 3% amount the buyer withheld, you must pay the remaining balance to the tax agency (AEAT) when you file your Modelo 210.

- Tax Owed is Less Than the 3% Retention (or You Made a Loss): If your tax bill is less than the 3% held back, or if you actually sold the property at a loss, you are due a refund from the tax office.

Here’s the key takeaway: Even if you sell at a loss, the buyer must still withhold and pay the 3%. The only way to get that money back is to file Modelo 210, formally declare the loss, and request the refund.

If a refund is due, the processing time depends on the tax office handling the file and on whether the supporting documents are complete from the outset. It is better to treat the refund as an administrative process with variable timing rather than promise a fixed outcome.

Navigating the Modelo 210 filing and making sure every deduction is properly applied can be a real headache. We handle this process for clients across Spain every day. Contact us for personalised advice, and we’ll make sure it’s done right.

Key Tax Considerations for Foreign Property Owners

When foreigners buy or sell property in Spain, we see the same issues trip them up time and again. Overlooking these fundamentals leads to delays, unexpected costs, and a lot of headaches. Getting them right from the start is the key to a smooth transaction.

First, the NIE number (Número de Identificación de Extranjero). You absolutely can’t buy or sell property, or file taxes like AEAT Modelo 211, without one. It’s non-negotiable for both the buyer and the seller.

Fiscal Representation and Annual Taxes

We always advise non-resident clients to appoint a fiscal representative in Spain. This isn’t just about convenience; it’s about compliance. Your representative becomes your official point of contact with the Spanish Tax Agency (AEAT), managing all filings like Modelo 211 and ensuring you never miss a deadline.

This brings us to your annual tax duties. Even if you never rent out your Spanish property, you are still required to file Modelo 210 every year for imputed income tax. This is a tax on the benefit of simply owning the property, and it catches many foreigners by surprise.

This imputed income is calculated based on your property’s cadastral value, multiplied by either 1.1% or 2%. That resulting amount is then taxed at a rate of 19% for EU/EEA residents or 24% for everyone else. It’s an ongoing cost of ownership that applies to everyone, from retirees to digital nomads.

Legal Diligence and Special Statuses

For any foreign buyer, conducting thorough legal due diligence is a critical step. This is how you uncover hidden debts, planning problems, or legal issues tied to the property before you sign anything. It’s a small investment that can save you from huge, costly problems later on.

A question we hear a lot is, “Does my special tax status, like the Beckham Law, change how property sales are taxed?” The short answer is no.

Property capital gains are taxed under the general rules, not the favourable rates of the Beckham Law regime. The standard tax rules for property apply equally to everyone. Whether you’re a digital nomad, a retiree, or a Beckham Law beneficiary, the obligations around a sale—like the 3% retention and the final capital gains declaration—are exactly the same.

If you’re trying to figure out how all this applies to your specific situation, it’s easy to feel overwhelmed. Contact us for personalised advice, and we’ll make your obligations clear.

Common Questions About Modelo 211 and Property Sales

What Happens If the Buyer Fails to File Modelo 211?

This is a mistake buyers can’t afford to make. If you buy a property from a non-resident and fail to withhold the 3%, or you withhold it but don’t pay it to the tax office (AEAT) with Modelo 211, the problem becomes yours.

The AEAT can pursue the buyer under the applicable rules, and the property remains affected in the legal terms tied to the retention and the corresponding tax debt. It is a serious issue, but it should be explained with the correct scope rather than as an automatic blanket lien for any amount.

Can the Seller Get the 3% Retention Back After a Loss?

Yes, absolutely. This happens all the time.

Even if you sell your property for less than you bought it for, the buyer is still required by law to withhold the 3% and submit it via Modelo 211. The retention is not optional; it has nothing to do with whether you made a profit or not.

To get your money back, you have to file a Modelo 210 tax return. This is where you formally declare the capital loss. Once the tax office reviews your documents and confirms you sold at a loss, you’re entitled to a full refund of the retained amount—that’s €9,000 on a €300,000 sale.

The key point: The tax office won’t automatically refund your money. The only way to get the 3% back is to file a Modelo 210 and formally request it.

How Long Do Refunds from the AEAT Usually Take?

There is no single official turnaround time that can safely be promised in every case. The pace depends on the AEAT office handling the file and on whether the documentation is complete and internally consistent.

The practical lesson is not to rely on a fixed number of months, but to prepare the Modelo 210 refund file carefully from the start so the review is not delayed by avoidable defects.

Is It Necessary to Hire a Tax Advisor for This Process?

You can technically file the forms yourself, but we strongly advise against it, especially if you’re not a resident.

The Spanish tax system is a minefield of complexities, and the forms are only in Spanish. A simple error—a wrong NIE, a bad calculation, a missed deadline—can trigger fines and turn a simple process into a nightmare.

Hiring an expert to manage the AEAT Modelo 211 for the buyer and the Modelo 210 for the seller is about peace of mind. It ensures everything is filed correctly, on time, and without errors. It saves you money in the long run.

Whether you’re buying or selling in Spain, the tax side of things can be intimidating. Our team handles this entire process for clients nationwide, from filing the Modelo 211 to reclaiming the 3% retention.

Contact us for personalised advice and let us handle the bureaucracy so you can focus on what matters.