The Non-Lucrative Visa Spain regime is the residence pathway designed for non-EU nationals who can sustain themselves financially in Spain without performing economic activity in Spanish territory. Its legal basis sits in the Ley Orgánica 4/2000 and is developed today in the Real Decreto 1155/2024, in force since 20 May 2025. The route is widely associated with retirees, but in practice serves a broader profile: investors living off passive income, families on extended sabbatical and high-net-worth individuals using the NLV as a strategic entry point before transitioning to other authorisations.

This article addresses the legal nature of the visa under the new Reglamento, the substantive requirements that drive most refusals, the strategic comparison with the Digital Nomad Visa, the renewal calendar, and the tax consequences that follow once Spanish residence is consolidated. The recurring causes of denial are concentrated in a small number of patterns that are visible to the consulate before the merits of the file are even examined.

Legal nature of the visa under the new Reglamento

The Non-Lucrative Visa authorises residence in Spain for non-EU nationals on the substantive condition that the applicant does not perform any economic activity, employment or self-employment in Spanish territory. The non-lucrative qualifier is absolute in its formulation: the residence is granted on the assumption that the applicant’s livelihood comes from sources unrelated to active work performed in Spain. The risk of misclassification is real for applicants who maintain remote work for foreign employers, because the operational interpretation by some consular offices may treat such activity as inconsistent with the non-lucrative status, even when the work is performed exclusively for non-Spanish counterparts.

For applicants whose income source is active remote work, the legally aligned pathway is typically not the NLV but the residence framework for displaced professionals or remote workers, where the activity is part of the authorised purpose. The strategic choice between regimes is therefore a substantive decision that conditions the entire file from the outset.

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

Who realistically qualifies

The profile most commonly associated with the NLV is the retired non-EU national with reliable pension income. The actual range of applicants is broader: investors with documented portfolio income, families on a year of cultural immersion, executives between roles with substantial liquid resources, and individuals testing residence in Spain before committing to a different authorisation more aligned with their economic structure.

The common denominator is the absence of active economic activity in Spain combined with documented financial autonomy. Beyond that, the consular evaluation focuses on the coherence of the applicant’s narrative with the documentary record.

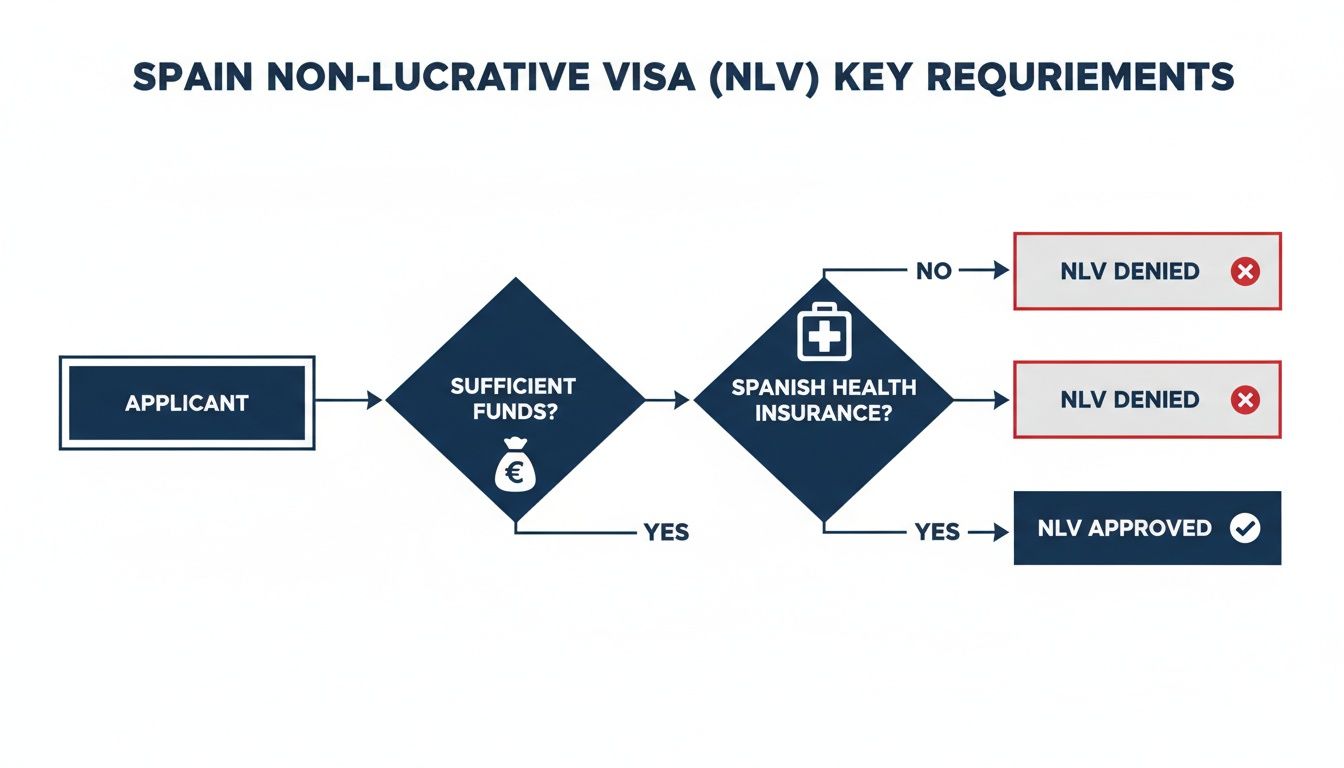

Financial requirements — the IPREM threshold and the stability test

The financial requirement is anchored on the Indicador Público de Renta de Efectos Múltiples (IPREM) in force for the year of the application. The applicable thresholds are four hundred per cent of the annual IPREM for the main applicant and one hundred per cent of the IPREM for each additional family member. The euro equivalent shifts when the IPREM is revised, but the percentages are stable.

Meeting the numerical threshold is a necessary but not sufficient condition. The substantive test that the consulate applies is the stability and verifiability of the income or savings. Refusals concentrate in three recurring patterns: funds whose legal origin cannot be traced through banking records, income flows that lack a consistent multi-year history, and documentary structures that present the financial position fragmentarily rather than as a coherent whole. Practical considerations for the banking infrastructure of the application are addressed in our note on opening a Spanish bank account.

The financial test is not a snapshot. The consulate reads a trajectory and looks for inconsistencies between the declared lifestyle, the income source and the documentary chain. A file that is technically compliant but documentarily fragmented is read as fragile.

Healthcare coverage requirement

The applicant must contract private health insurance with an entity authorised to operate in Spain, with cover equivalent to that provided by the Spanish national health system. The operational standards that consulates apply are strict: policies with copayments, with material exclusions or with carence periods that leave the applicant uncovered during the validity of the visa are routinely rejected. Travel insurance and foreign health plans, however broad, do not satisfy the requirement.

The healthcare requirement is one of the most frequent causes of refusal precisely because applicants tend to underestimate the specificity of the standard. The cleanest position is to contract the policy with a Spanish-authorised insurer using a product specifically designed for the residence application.

Non-Lucrative Visa versus Digital Nomad Visa — the strategic decision

The choice between the NLV and the Digital Nomad Visa is one of the most consequential strategic decisions in the file. The structural difference is absolute: the NLV prohibits any economic activity in Spain, including remote work for foreign employers under the strictest consular reading; the DNV is the regime designed precisely for remote workers serving non-Spanish clients or employers.

The wrong choice at this stage is not corrected by a subsequent file. A refusal under the NLV because the applicant has active remote work generally implies restarting under the DNV with the time and documentary cost that this entails. The detailed contrast with the DNV is developed in our note on the Digital Nomad Visa one year after its implementation.

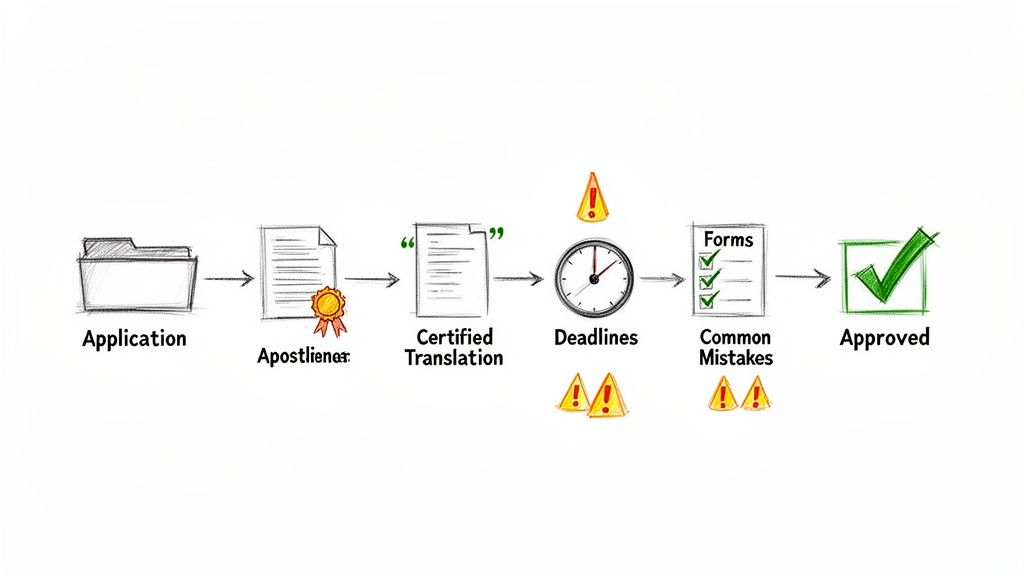

Application process and recurring refusal patterns

The application is filed at the Spanish consulate of the applicant’s place of residence. The procedural sequence is unforgiving: the documentary chain must be assembled in the correct order, with the legalisations and translations executed before the validity windows of the underlying certificates expire.

The recurring causes of refusal cluster in the same areas across consulates.

For applicants who arrive at our practice after a refusal, the underlying eligibility is usually present. What was missing is the strategic structuring of the file. The recurring lesson is summarised in our note on the most common mistakes when moving to Spain.

Renewal calendar and the path to long-term residence

The initial visa typically grants residence for one year. The first renewal requires evidence of substantive permanence in Spanish territory during that year, with the operating threshold of one hundred and eighty-three days as the central reference. After the first renewal, the authorisation is granted in two-year periods.

After five years of legal continuous residence, the applicant can transition to long-term residence under the framework of articles 175 to 189 of the Real Decreto 1155/2024. Long-term residence is the milestone that ends the structural restriction of the NLV on economic activity, opening access to employment and self-employment under conditions equivalent to those of Spanish nationals within the foreign nationals’ regime. The interaction between the NLV calendar, modification to a work authorisation after the first year, and the eventual transition to long-term residence is one of the strategic axes of the file.

The tax consequences of becoming Spanish resident

The grant of the NLV brings with it the consolidation of the applicant’s situation as a Spanish tax resident, with the consequent obligation to declare worldwide income under the IRPF. For applicants with international assets, this transition activates a series of substantive obligations: the IRPF on worldwide income, the Impuesto sobre el Patrimonio (or, where applicable, the Impuesto Temporal de Solidaridad de las Grandes Fortunas) and the informative obligations on assets held abroad.

Unlike the DNV, the NLV does not by itself trigger access to the special regime of the displaced worker under article 93 LIRPF. Tax planning before relocation is therefore not optional for applicants with material asset positions. The correct sequencing of relocation, fiscal residence acquisition and structuring of the asset position can have a determining impact on the tax cost of the move.

When professional guidance for the Non-Lucrative Visa Spain matters most

Some applications are operationally simple and substantively defensible without intervention. Others require strategic preparation from the outset.

Legal advice is decisive when the applicant maintains any form of remote work that the consulate could reread as incompatible, when the income source is structured (passive vehicles, foreign trusts, complex investment arrangements), when the family unit includes situations of complex dependence or international custody, when there is any prior immigration record requiring contextualisation, or when the strategic intent is to use the NLV as an entry point for a subsequent transition to a work authorisation or to long-term residence.

In these cases, the value of legal preparation is not in the form filling. It is in the architecture of the file: deciding which regime to invoke, when to file, how to present the financial position, how to coordinate the visa with the tax planning, and how to anticipate the renewal milestones from day one.

Frequently asked questions

Can I work remotely on the Non-Lucrative Visa Spain?

The Non-Lucrative Visa is incompatible with active economic activity, and the consular interpretation extends to remote work for foreign employers under the strictest reading. The defensibility of any factual situation that includes ongoing remote work depends on the overall consistency of the applicant’s position and is generally weaker than transitioning to the Digital Nomad Visa, which is the regime designed for remote work.

How much money do I need to qualify financially?

The legal threshold is four hundred per cent of the IPREM in force for the year of the application for the main applicant, plus one hundred per cent of the IPREM for each additional family member. Meeting the numerical threshold is necessary but not sufficient: the consulate evaluates the stability and the documentary verifiability of the financial position. The defensibility rests on early documentation of the income trajectory and the legal origin of the funds.

How long does the application take in practice?

The processing times vary materially by consulate and by season. Realistic planning assumes several months from documentary preparation to consular decision. The practical answer still requires confirming the operational situation of the consulate of the applicant’s place of residence, since the same regime is processed under different administrative rhythms across jurisdictions.

What are the most common reasons for refusal?

The recurring patterns are documentary sequencing failures, financial proof presented as fragmentary balances rather than as a documented trajectory, healthcare policies that do not meet the standard expected by the consulate, and inconsistency between the applicant’s factual situation and the non-lucrative qualification. The defensibility of any subsequent application depends on the technical analysis of the original refusal and the strategic restructuring of the file before re-presentation.

Can I switch from the Non-Lucrative Visa to a work authorisation later?

Yes. After the first year of legal residence under the NLV, the regime allows modification to a work authorisation, subject to the substantive requirements of the destination authorisation. The strategic question is when and how to execute the modification, since the timing and the documentary preparation determine the success rate. The defensibility rests on early planning of the modification rather than on a reactive request after the first year.

Conclusion — eligibility is not the same as a defensible file

The Non-Lucrative Visa Spain remains one of the most accessible residence pathways for non-EU nationals with documented financial autonomy, but it is also one of the most frequently refused, because the gap between meeting the formal threshold and presenting a defensible file is wider than most applicants assume. Recurring refusals concentrate in patterns that can be anticipated and prevented at the preparation stage.

If a Non-Lucrative Visa application is in your near horizon, the most useful step is a strategic review that identifies the right regime (NLV versus DNV versus alternative pathways), the documentary sequencing, the financial structuring and the tax planning before the file is submitted. Legal Fournier advises international clients on Spanish immigration and tax matters, including NLV preparation, refusal recovery and transition strategy to subsequent authorisations.

Legal Disclaimer. This article is for informational purposes only and does not constitute legal advice. Every case involves specific facts and circumstances that may affect the outcome under the Real Decreto 1155/2024, the Ley Orgánica 4/2000 and the Ley 35/2006 del IRPF. Legal Fournier recommends seeking professional legal guidance before taking any action based on the information contained in this article.