An outdated company tax address in Spain is rarely just an administrative detail. For a Spanish company, especially a foreign controlled SL, the more dangerous issue is usually invisible: AEAT may already be notifying the company electronically, the notice may be deemed rejected after the legal access period, and the next document the directors see may be a sanction, a liquidation, or an enforcement step.

This is the narrow risk behind the broader notificacion AEAT topic. The general question is how Spanish Tax Agency notices work. The company question is sharper: who inside the business is actually watching the tax mailbox, who has authority to access it, and whether the tax domicile recorded with AEAT still matches the company that exists today.

For founders setting up a company in Spain, this should be treated as part of the company governance file from day one, not as a later accounting detail. Our company formation work therefore looks beyond incorporation documents and asks how the company will receive, escalate, and answer official tax communications once it is active.

Last updated: 2 June 2026

- Spanish legal persons, including companies, are generally obliged to deal electronically with public administrations under article 14 of Ley 39/2015.

- Electronic notices are usually effective when accessed, or treated as rejected after 10 calendar days if access is required and nobody opens them.

- For companies and other entities, a change of tax domicile must generally be communicated through the census modification route within one month.

- A missed AEAT request can create a separate sanction risk for not attending a duly notified requirement.

- Changing the registered office, changing accountant, or forwarding email alerts is not enough unless the AEAT census, DEHú access, powers, and response workflow are also controlled.

Why this risk Is different for A company

Individuals often think about tax notices as letters. Companies should think about them as procedural events. A notice is not simply information arriving in a mailbox; it is the event that can open a deadline to answer, pay, allege, appeal, or correct a filing. If the company does not see the notice, the legal clock may still move.

The starting point is the domicilio fiscal. Article 48 of the Ley General Tributaria defines the tax domicile as the location of the taxpayer for its relations with the tax administration. The same provision says taxpayers must communicate their tax domicile and changes to it, and that a change does not produce effects before the tax administration until the communication duty has been fulfilled.

That is the first trap for foreign controlled companies. The commercial address, the registered office, the accountant’s office, the director’s home, and the tax domicile can become confused. A group may move management from Madrid to Barcelona, a property-holding company may stop using the original adviser, or a founder may leave Spain after incorporation. If the census record is not updated, AEAT may still read the company through stale data.

For companies and other entities, the census route matters. Article 10 of Royal Decree 1065/2007 states that the declaration of modification serves, in particular, to communicate a change of tax domicile for legal persons and other entities. Article 17 of the same regulation provides the one-month communication period for legal persons and entities, and says that in the state tax sphere the communication is made through the census modification declaration.

In practice, that usually means a Modelo 036 or the corresponding electronic census procedure. The AEAT guidance on the deadline for census modification declarations also describes the general one-month period for Modelo 036 modification filings, with specific exceptions for certain cases.

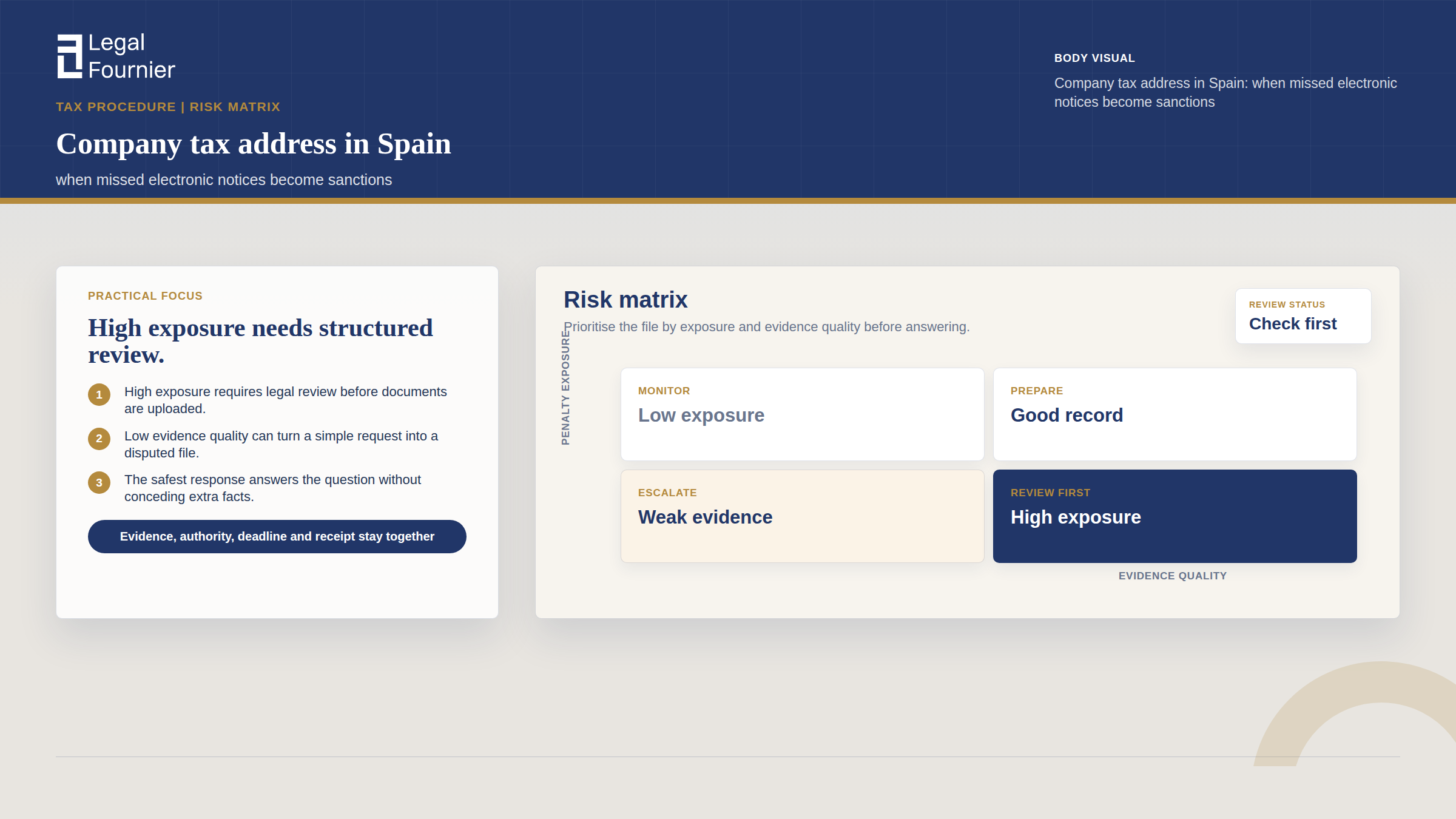

Practical rule: a company address update is not finished when the lease, notary deed, or website footer changes. It is finished when the tax census, electronic notification access, powers of representation, and internal response owner all match the real company.

Need help with your case in Spain?

If this article applies to your situation, contact our team for tailored legal guidance and clear next steps.

Electronic notices: the 10-day problem

The second trap is that companies are not waiting for the same paper-notice system that many foreign directors imagine. Article 14 of Ley 39/2015 includes legal persons among those obliged to relate electronically with public administrations for administrative procedures. Article 43 of the same law regulates electronic notifications through the relevant electronic office or the Dirección Electrónica Habilitada Única, commonly called DEHú.

The difficult sentence is in article 43: when electronic notification is mandatory, or has been expressly chosen, the notification is understood as rejected once 10 calendar days have passed from being made available without access to its content. AEAT’s own electronic notifications FAQ explains the same practical effect for tax notices: access produces the notification, and if access does not happen, the passage of the 10-day period can produce the legal effect.

This is why “we did not receive the email” is usually the wrong defence. AEAT and DEHú offer alert systems, but the alert is not the legal notification itself. The official event is the notice made available in the electronic system and the access, or deemed rejection, recorded by that system. The AEAT FAQ also notes that access can be made through the AEAT electronic office or DEHú, and that the system records dates and times for availability, access, and deemed rejection.

For a company, the operational question is therefore not whether someone noticed an email. It is whether the company, a valid representative, or an expressly empowered person can access the notice in time and pass it to the person who can make a legal decision. A certificate belonging to a former sole director, an accountant without the right power, or a mailbox monitored only during monthly bookkeeping is a weak control for a 10-calendar-day legal clock.

How A missed notice becomes A sanction

Not every missed notice automatically becomes a sanction. Spanish tax sanctions require a legal basis and, under article 183 of the Ley General Tributaria, an intentional or negligent action or omission that is classified and sanctioned by law. That caveat matters. A late discovery of an AEAT notice should be analysed before anyone assumes the worst.

But the risk is real because the missed notice can be the first step in a chain. A common sequence looks like this:

- AEAT issues an electronic requirement, proposal, liquidation, or sanction initiation document.

- The company does not access the notice within the electronic access period.

- The notice is treated as rejected or effective for procedural purposes.

- The response, payment, allegation, or appeal period begins to run.

- The company misses the deadline because nobody knew the document existed.

- AEAT continues the file, and the company may face a sanction, a final assessment, executive-period surcharges, or enforcement action.

The most direct sanction risk often appears when the missed document was a requerimiento, a formal request for information, documents, accounting records, invoices, attendance, or explanation. Article 203 of the Ley General Tributaria treats resistance, obstruction, excuse, or refusal to tax administration actions as a serious infringement and expressly includes not attending a duly notified requirement.

The same article sets fixed sanctions for certain unattended requirements and higher sanctions where the request concerns documents, books, files, invoices, accounting records, systems, attendance, access, or information with tax relevance in economic activity cases. The numbers depend on the type of requirement, the stage of the procedure, repetition, and whether the taxpayer later complies. This is where specialist review changes the outcome: the issue is not only “was there a notice?” but what was notified, whether the notice was valid, what deadline followed, what evidence exists, and what response can still be made.

A different chain arises where the missed notice is a liquidation or debt document. Article 62 of the Ley General Tributaria sets payment periods for debts resulting from administrative liquidations. Article 161 says the executive period starts, for debts liquidated by the administration, the day after the article 62 payment period expires. Article 28 then regulates executive-period surcharges. In plain terms: missing the notification can mean missing not only the argument window but also the voluntary payment window.

The four weak points we see in foreign-owned companies

The companies most exposed are not necessarily careless companies. They are often foreign controlled businesses with international management, a part-time accounting provider, and no single person who owns the AEAT notice process.

| Weak point | Why it creates risk | Typical result |

|---|---|---|

| Old fiscal address | The company moved, but the census record was not updated or was updated late. | AEAT records and territorial files do not match the current business reality. |

| Expired or misplaced certificate | Only a former administrator or old provider can access the electronic mailbox. | Notices sit in DEHú while the directors believe the company has no open file. |

| Unclear accountant mandate | The provider files quarterly returns but is not expressly empowered to receive or answer notifications. | A document is downloaded but not escalated, or nobody is legally able to respond. |

| No holiday or absence protocol | A 10-calendar-day period can run during travel, August, acquisition closing, or director absence. | The company discovers the issue only when a later sanction or enforcement notice appears. |

These weak points are easy to underestimate after a smooth incorporation. A company may have a Spanish NIF, a bank account, an accountant, and a registered office, yet still lack a reliable official-notice workflow. That is why ongoing compliance support, not just the initial deed, matters. See also our monthly accounting service for the operational side of Spanish company compliance.

What to verify when A company moves address

A company address move should trigger a controlled compliance checklist. The checklist should not be left to the last person who touched the lease or the website.

1. separate registered office from tax domicile

The domicilio social and domicilio fiscal may coincide, but they should not be treated as automatically identical in every file. A change at the notary or Commercial Registry does not replace a tax census review. If the effective management, business administration, or tax-relevant contact point changed, review whether the Modelo 036 or census data must be amended.

2. confirm the AEAT census record, not just internal records

The company should verify what AEAT actually shows for the company: fiscal address, notification contact details, representatives, activity status, VAT or intra-community positions where relevant, and census obligations. If the company is in a wider group, do not assume the group address or local office address is the address AEAT has recorded.

3. test who can access dehú and AEAT notices

Access is a legal-control issue, not an IT convenience. Check who holds the company representative certificate, whether it is valid, whether a new administrator needs a new certificate, and whether a third party has an express AEAT power to receive electronic notifications. AEAT’s FAQ states that the content of electronic notifications can be accessed directly by the taxpayer or by a proxy with express power for electronic notifications.

4. do not rely on alert emails as the compliance system

Alerts are useful, but they are not the legal notice. They can fail, land in spam, go to a former employee, or be ignored during travel. The compliance system should be based on active, scheduled checks of AEAT and DEHú, with documented escalation rules when a notice is found.

5. use AEAT courtesy days where appropriate

AEAT allows users included in electronic notification systems to designate up to 30 calendar days per year during which AEAT will not make electronic notices available, subject to the conditions of the procedure. AEAT’s courtesy-days guidance says they must be requested at least seven calendar days before the start of the chosen period. This is useful for holiday and shutdown planning, but it does not repair notices already made available before the courtesy period begins.

If you have already found A missed AEAT notice

If the company has already discovered an expired electronic notice, the worst response is a generic letter saying “we did not know.” The first task is forensic: reconstruct the file before deciding the legal move.

Start by identifying the exact document: was it a request for information, a proposed liquidation, a final liquidation, a sanction initiation, a sanction resolution, a payment demand, a providencia de apremio, or another procedural act? The answer changes the available remedy. Then identify the notice date, the date it was made available, the access date or deemed rejection date, and every deadline that followed.

For appeals, the calendar can be unforgiving. Article 223 of the Ley General Tributaria sets a one-month period for the administrative reconsideration remedy known as recurso de reposición, counted from the day after notification of the appealable act. Article 235 sets a one-month period for the economic-administrative claim in first or single instance. The correct route depends on the act, the tax involved, the stage of the file, and whether the company is trying to suspend collection, challenge the merits, attack the notification, or repair compliance.

Where the deadline has passed, the analysis becomes more delicate. There may be narrow arguments around notification validity, access authority, procedural defects, impossibility, lack of culpability, or later remedies, but these are fact-sensitive and should not be treated as standard templates. The company should preserve screenshots, certificates, DEHú records, powers of attorney, email alerts, accounting communications, and any evidence showing who could or could not access the notice.

Legal strategy point: the question is not only whether the company missed the notification. It is whether AEAT can prove a valid notification chain, whether the resulting deadline was correctly applied, and whether the sanction file properly addresses responsibility and the company’s actual conduct.

Governance rule: name the owner of the tax mailbox

For an active Spanish company, the cleanest prevention rule is simple: one named person or team must own the official tax mailbox. That owner does not need to make every legal decision alone, but must be responsible for checking, recording, escalating, and confirming the response route.

A serious company should keep a written notice protocol covering at least these points:

- Who holds the representative certificate and when it expires.

- Who has express AEAT power to access electronic notifications.

- How often AEAT and DEHú are checked, with backup coverage during holidays and travel.

- Which director, adviser, or legal team receives each category of notice.

- How deadlines are logged and confirmed.

- Who is responsible for updating Modelo 036 or census data after address, director, activity, or group changes.

For foreign investors, this is particularly important after company formation, acquisition of a Spanish company, change of administrator, relocation of operations, change of accounting provider, or change from a dormant to active business. Those are the moments when official-notice control often breaks.

There is no premium value in discovering a sanction late. The value is in building a company file that makes late discovery unlikely: tax domicile aligned, powers current, certificate valid, notices monitored, and legal review triggered before the deadline is almost gone.

FAQ

Is an AEAT email alert the official notification?

No. Alerts are useful operational warnings, but the legal notification is made through the official electronic system, such as AEAT’s electronic office or DEHú, according to the applicable procedure. A failed or missed alert does not usually stop the legal notification clock by itself.

Can a company be sanctioned if nobody opened the electronic notice?

It can happen. If the company is obliged to receive electronic notifications and a notice is validly made available, the law can treat it as rejected after the 10-calendar-day period without access. Whether the resulting sanction is defensible depends on the specific act, evidence, procedure, and responsibility analysis.

Does changing the registered office update the AEAT tax address?

Not safely by itself. A company should separately verify its AEAT census data and, where required, file the corresponding census modification. For legal persons and entities, the general regulatory period for communicating a change of tax domicile is one month from the change.

Can my accountant open and answer AEAT notices for the company?

Only if the access and authority are properly in place. Filing tax returns is not the same as holding an express power to receive electronic notifications or to make legal decisions in a tax procedure. The exact power, certificate, engagement scope, and escalation protocol should be checked.

What should we do after finding an expired AEAT notice?

Download the full file, preserve the electronic notification evidence, identify the act and deadlines, and obtain legal review before sending a generic explanation. The available route may be very different depending on whether the file is still in the response period, appeal period, sanction stage, or executive collection stage.

Legal Disclaimer. This article is provided for informational purposes only and does not constitute legal advice. Every case involves specific facts and circumstances that may affect the outcome. Legal Fournier recommends seeking professional legal guidance before taking any action based on the information contained herein.